Some of the costliest real estate mistakes I see have nothing to do with the house itself and everything to do with what happens after the sale.

In this episode, I sit down with Susan W. Jones of Sorelle Wealth Partners co-founder, an attorney, wealth advisor, and tax specialist who guides clients through major life transitions like divorce, retirement, and inheritance.

We get into the tax traps that ambush property owners, how to protect what you have built, and why a plan beats panic every time. This is for homeowners, real estate investors, and anyone who wants their property decisions to build wealth instead of quietly draining it.

Watch the full video here:

Why I Had This Conversation

In my world, the sale is the finish line. In Susan's, it is where the real financial questions begin, and that gap is exactly why I wanted her on the show.

Susan is a licensed attorney and wealth advisor who started in corporate law, fell in love with tax, and built a career helping high-net-worth clients through major life transitions. As Managing Partner and co-founder of Sorelle Wealth Partners, she blends legal, tax, and estate planning expertise with the kind ofhonest guidance on building real wealth I value in a coaching-oriented advisor.

What I appreciated most is how she reframes wealth management. It is not about picking stocks; it is about integrated planning that keeps more of what you earn.

"There's an expectation that wealth management is all about investments. The truth is the integration of financial planning, tax planning, and estate planning—that is such a core benefit."

– Susan W. Jones, Sorelle Wealth Partners

The Tax Traps That Ambush Property Sellers

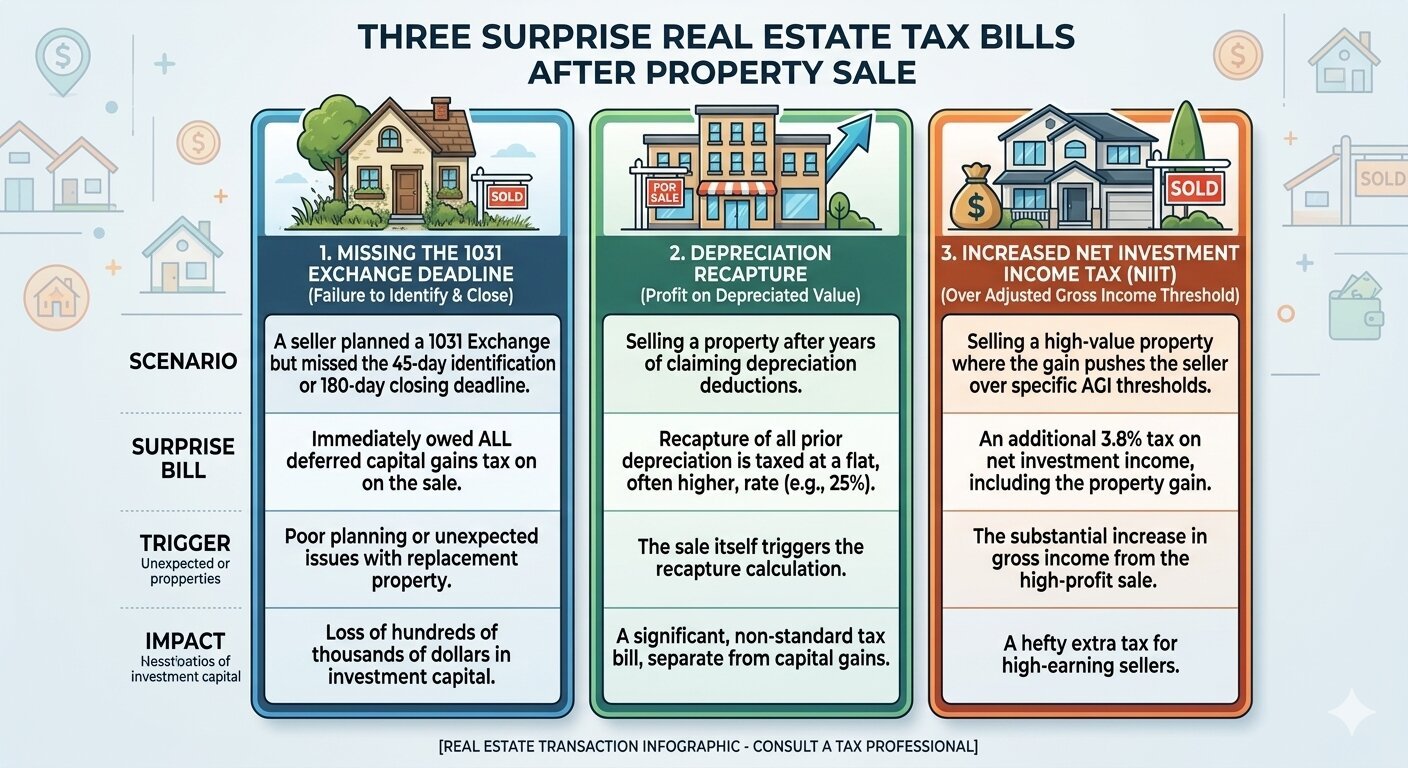

The first thing Susan drilled into me is that speed can be expensive. Real estate investors love to move fast, and that instinct, while powerful, can cost them dearly at tax time.

The biggest missed opportunity she sees is the 1031 exchange real estate strategy. Once you have taken the proceeds from a sale, it is too late to do one, so the window closes before many sellers even know it existed. A simple pause to call an advisor can preserve enormous value.

She also flagged two surprise bills people trigger without realizing it: state-level capital gains taxes on property held in a higher-tax state, and depreciation recapture, where the deductions that helped you for years lower your basis and enlarge your taxable gain at sale. Susan shares more in Sorelle'stax planning resources.

"The only thing worse than a tax bill is one that you didn't expect, like the day before it's due."

– Susan W. Jones, Sorelle Wealth Partners

The Inheritance Rule Everyone Should Know

This was the section I found most valuable for everyday families, because so many people inherit property in the middle of grief and make avoidable mistakes. Susan walked me through the stepped-up basis inheritance rule.

When you inherit property, the cost basis generally adjusts to the fair market value on the date of death. So if a parent bought a home for 400,000 and it is worth 600,000 when they pass, the heir's basis becomes 600,000, meaning little or no gain if sold right away. It is exactly the kind of nuance theteam at Sorelle Wealth Partners helps families plan for.

The practical tip we both loved: you usually do not need an expensive formal appraisal to establish that date-of-death value. A trusted real estate agent can pull comparable sales and email you a range for your file.

"As long as you still own it when you pass away, you have a basis adjustment, usually an increase to the fair market value on the date of death."

– Susan W. Jones, Sorelle Wealth Partners

That single stepped-up basis inheritance rule can save heirs a fortune, but only if they know to document the value before they sell.

Protecting Assets With the Right Structure

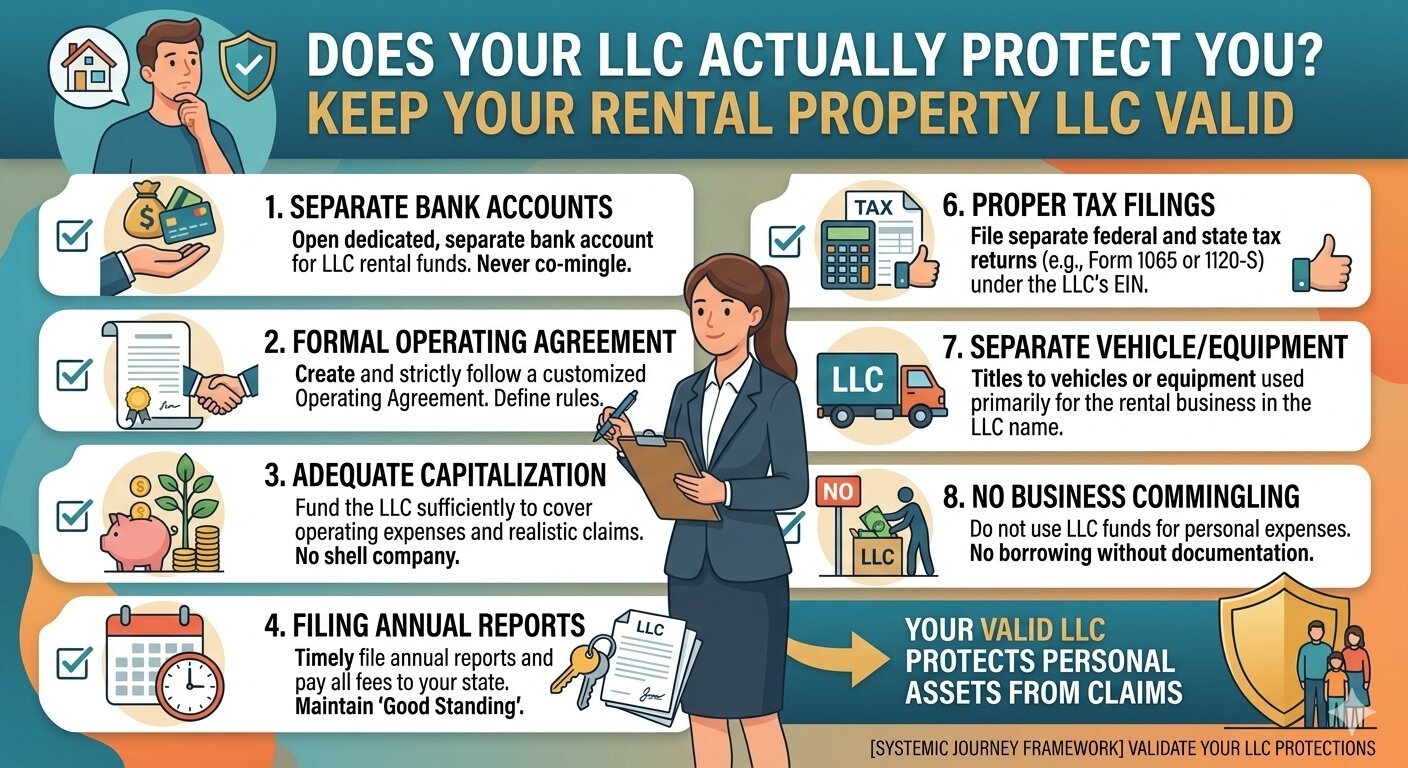

Susan was clear that selling inherited property taxes are only one piece; how you hold property while you own it matters just as much. Her top estate-planning priority for investors is liability protection.

For personal-use property, that often means titling it jointly with a spouse or in a joint trust. For anything you rent out, even occasionally, she recommends an LLC for rental property protection, with one major caveat: the structure only works if you respect it.

That meansseparating your personal and business finances through a dedicated bank account and, critically, making sure the insurance policy names the LLC as the owner. She also warned about mismatched or outdated deeds, sharing a sobering story of a hallmark family property that accidentally passed to an uncle because of an unupdated deed, sparking a dispute that landed a family member in the hospital.

What Changed for Me After This Conversation

"In order to have return, you have to have risk. Those two things just go together. So it's really a question of, if you want to grow your wealth, what can I do to mitigate risk but also have market returns?"

– Susan W. Jones, Sorelle Wealth Partners

That reframed how I talk about security with clients. Many people feel safest with cash they can touch, but Susan showed how money that only sits, never keeping up with inflation, is its own quiet risk. Real security comes from a plan, not a mattress.

I also rethought what it means to be wealthy in real estate. Being property rich is not the same as being financially free, and diversifying beyond real estate is what turns a portfolio into sustainable, accessible wealth.

Now I tell clients to stress-test their plan for the good years and the bad, and to surround themselves with people smarter than they are in each lane. For anyone weighing selling inherited property taxes against long-term goals, or simply diversifying beyond real estate, Susan's point lands: the goal is to be comfortable in the middle, okay even when times are not their best, the spirit behind theintentional wealth management Sorelle Wealth Partners brings to every client.

That is the mindset behind everything Susan W. Jones and Sorelle Wealth Partners brought to this conversation.

Common Questions From Property Owners

What is a 1031 exchange, and why do people miss it?

A 1031 exchange lets you defer capital gains taxes by reinvesting proceeds from one investment property into another. Susan stresses that once you have taken the sale proceeds, it is too late to do one, which is why so many investors miss the opportunity by moving too quickly.

What is a stepped-up basis when inheriting property?

It means the property's cost basis generally adjusts to its fair market value on the original owner's date of death. As Susan explains, if you sell shortly after inheriting, you may owe little or no capital gains tax because the basis reset to the current value.

Do I have to put all my home-sale proceeds into a new home to avoid taxes?

No. Susan notes this is an outdated rule many people still believe. Today there is a flat capital gains exclusion you can use periodically if you have lived in the home long enough, so reinvesting every dollar into another property is no longer required.

Why do I need an LLC for a rental property, and how do I keep it valid?

An LLC provides liability protection, but only if you respect the structure. Susan advises running income and expenses through a dedicated LLC bank account, obtaining a free EIN, and ensuring your insurance policy is titled in the LLC's name so coverage matches the true owner.

How can families avoid real estate becoming a burden for the next generation?

Susan recommends keeping titling, trusts, and beneficiary designations current, and adding real guardrails for shared properties like vacation homes. She cautions that leaving a property without funds for its upkeep, the roof, insurance, and operating costs, often creates family conflict later.

Found This Valuable? Don't Lose Touch.

One episode can't cover every way to protect what you have built. If tax strategy, inheritance, and estate planning spoke to you, stay connected with us.

💼 Connect with Susan Jones:

🌐 Website

🎧 Follow Deanna Brummett:

🌐 Website

Apply to Be a Guest on the Make Yourself at Home Podcast

Real estate touches every major financial decision a family makes, and the experts who help people navigate it deserve a wider audience. The best conversations I get to host are not just about buying and selling, they are about the planning, the protection, and the hard-won wisdom that keeps a family's wealth intact for generations.

That is exactly what this show is built for. Whether you help people minimize taxes, structure their estate, protect their assets, or simply make calmer decisions during a major life transition, your expertise could be the thing that saves a listener from a costly mistake they never saw coming.

If you work in wealth management, law, tax, real estate, or any field that helps people protect what they have built, I would love to have you on the show. Learn more about the Icons of Real Estate podcast network.