Most people do everything they’re told - save aggressively, fund the 401(k), pay down the house - and still end up financially fragile. In this episode of Make Yourself at Home, I sat down with Chris Miles of Money Ripples to talk about why that model is broken and what to do instead. Chris is a former financial advisor turned cashflow expert who rebuilt his own wealth from over a million dollars in debt - not once, but twice.

Here’s what we covered in our conversation:

-

Why traditional financial planning often fails even diligent savers

-

The danger of relying on appreciation instead of cashflow

-

How the get lean get liquid get out framework builds financial independence passive income

-

Where Chris invests for consistent monthly cash flow

-

How to start building income before you have capital to invest

Listen to the full episode:

Why I Had This Conversation

I got my real estate license in 2008 - right as the market was imploding. I didn’t walk into easy transactions. I walked into short sales, foreclosures, and families who had done everything right and still lost everything. I’ve sat at dining room tables with people in genuine financial crisis, trying to help them navigate forward. That experience never leaves you.

So when I connected with Chris Miles, founder of Money Ripples, I recognized someone who had been on the other side of that same equation. He wasn’t talking theory. He had lived the collapse, lost over a million dollars, and rebuilt financial independence twice. What he shared in our conversation challenged the way I think about the homes and Properties in Charlotte metro area, North Carolina that I help people buy and sell.

Why Traditional Financial Planning Often Fails

One of the first things Chris shared stopped me in my tracks. He described sitting down with his own father - a man who had done everything by the book for decades. Paid off all his debt. Maxed out his 401(k). Never spent a dollar he didn’t have to. And after all of it, Chris ran the numbers and told his father he would run out of money within five or six years of retiring.

His dad had done everything right. And it still wasn’t enough.

"My dad was the person who taught me to save everything and spend nothing, so I figured I should be able to help him retire. I sat down with him and said, ‘Dad, you’re 61 years old. You paid off all your debt. You’ve stuffed money in your 401(k). After all the decades of savings, if you try to retire today, you’ll need to die in about five or six years, because you’ll run out of money.’ He said, ‘Well, that’s not why I’m here, Mr. Sunshine.’ And that bothered me so badly that just a month later, I started asking whether this whole model actually works."– Chris Miles, Founder of Money Ripples

That experience led Chris to take stock of roughly one hundred advisors in his office - some there since the 1970s - and realize not one was financially free from the investments they were selling. Financial advisors don’t get paid to recommend alternative income streams, so they don’t.

One of the biggest wake-up calls for me was realizing just how many people are still financially dependent even after decades of “doing the right thing.” According to a 2025 Bankrate report showing 52% of Americans expect to rely on Social Security for essential retirement expenses, showing just how fragile conventional planning has become.

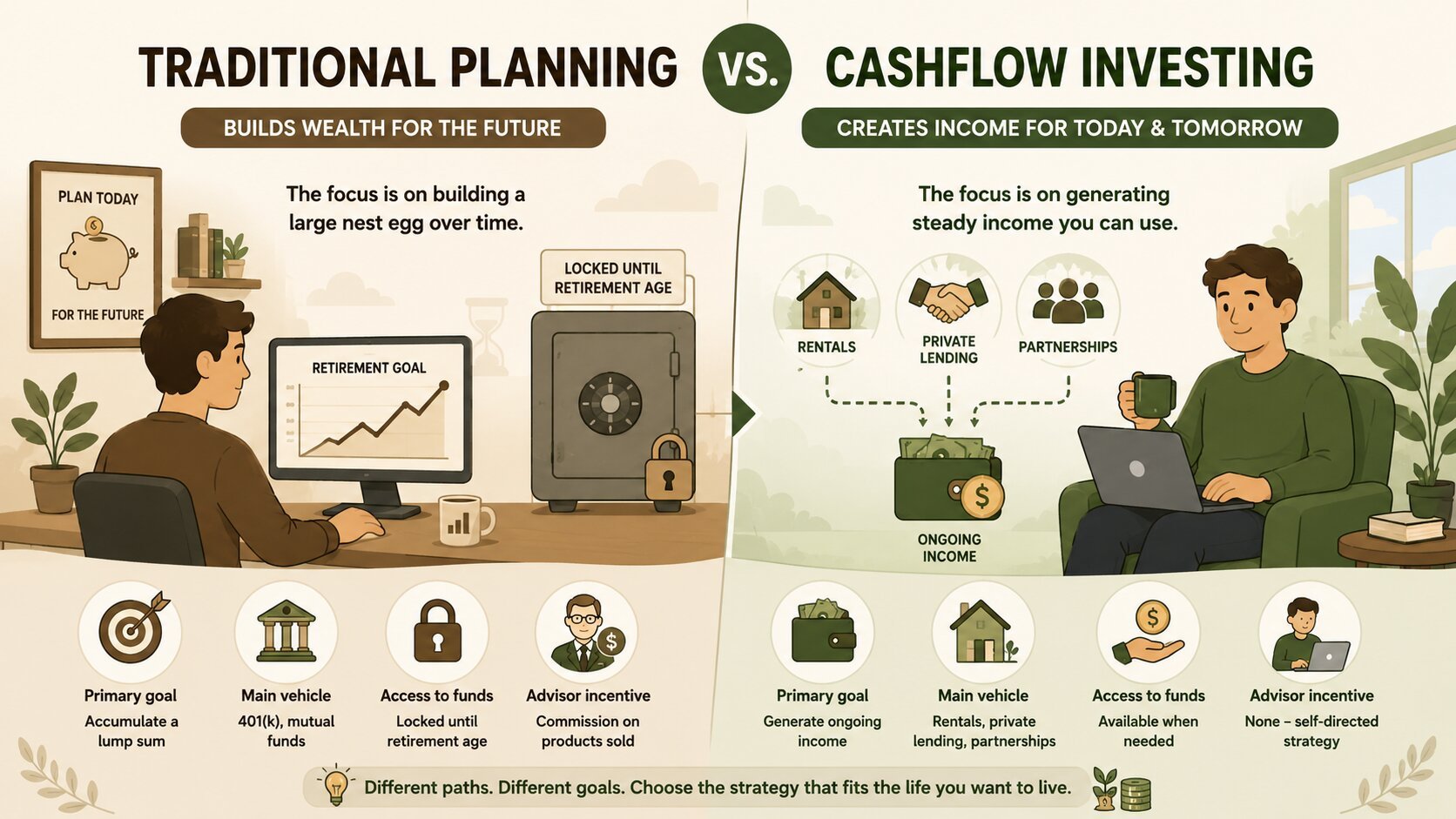

Traditional Planning vs. Cashflow Investing

Here’s a breakdown on the difference between traditional planning and cashflow investing. There is no right or wrong approach, but the key here is to understand which one fits the lifestyle that you want.

|

Metric |

Traditional Planning |

Cashflow Investing |

|

Primary goal |

Accumulate a lump sum |

Generate ongoing income |

|

Main vehicle |

401(k), mutual funds |

Rentals, private lending, partnerships |

|

Access to funds |

Locked until retirement age |

Available when needed |

|

Advisor incentive |

Commission on products sold |

None - self-directed strategy |

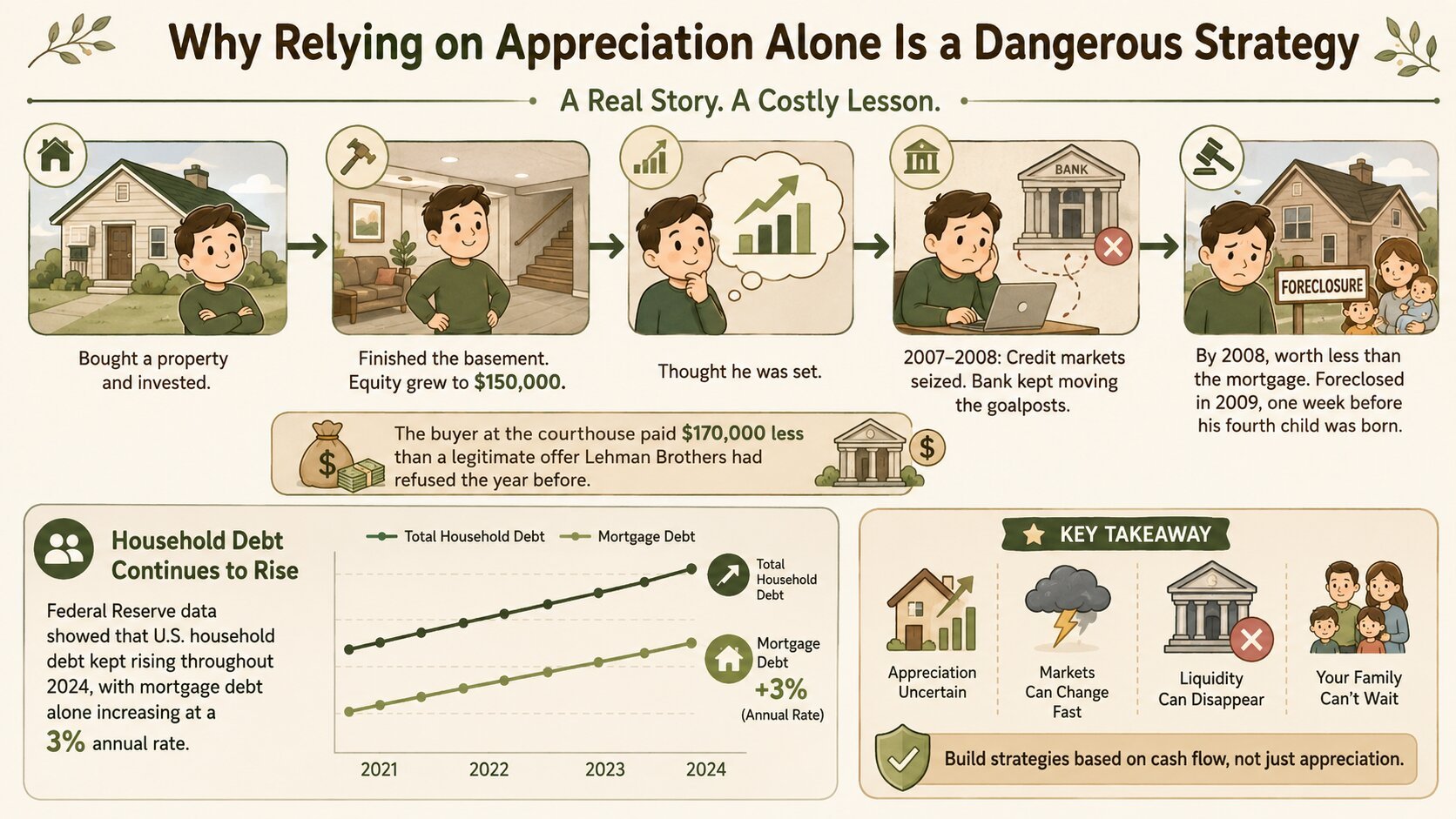

Why Relying on Appreciation Alone Is a Dangerous Strategy

This part of our conversation hit closest to home. As a real estate professional in Charlotte, I’ve watched clients make or lose significant money based entirely on whether the market cooperated with their timeline. Chris shared a story every homeowner needs to hear.

He bought a property, finished the basement, watched his equity grow to $150,000, and thought he was set. Then the credit markets seized in 2007. He tried to cash out that equity, and the bank kept moving the goalposts. By 2008, the home was worth less than the mortgage. He foreclosed in 2009, one week before his fourth child was born. The buyer at the courthouse paid $170,000 less than a legitimate offer Lehman Brothers had refused the year before.

The pressure on household finances continues to build. Federal Reserve data showed that U.S. household debt kept rising throughout 2024, with mortgage debt alone increasing at a 3% annual rate - making liquidity and cashflow investing strategies more important than ever.

His takeaway, and now mine:

-

Appreciation is a bonus, not a strategy

-

Equity locked in a home is equity you cannot access when markets turn

-

The investors who thrived in 2008 had profitable rentals - not the most equity

-

Over-funding a mortgage or 401(k) creates the same trap: you lose control of the money

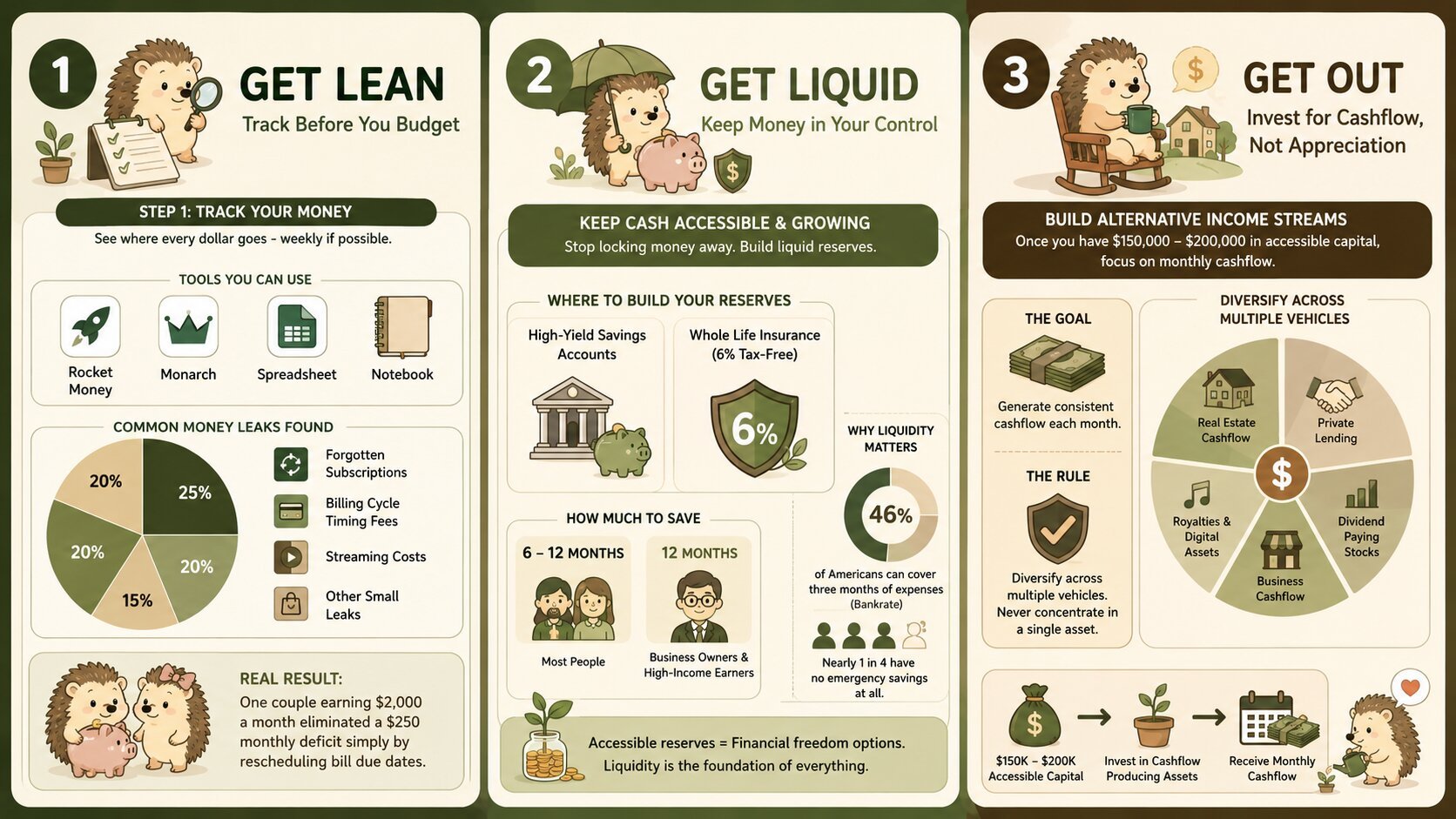

The “Get Lean, Get Liquid, Get Out” Framework

Chris built his entire roadmap for financial independence passive income around three phases, which he details in his book, the work optional blueprint. These are the exact steps he used to rebuild from over a million dollars in debt, and the same steps he walks clients through today.

Phase 1: Get Lean - Track Before You Budget

Most people start with a budget. Chris says that’s step two. Step one is tracking where your money actually goes - weekly if possible - using an app like Rocket Money, Monarch, a spreadsheet, or even a notebook. He’s found money leaks in virtually every client: forgotten subscriptions, billing cycle timing fees, streaming costs that crept to $300 a month unnoticed. One couple earning $2,000 a month eliminated a $250 monthly deficit simply by rescheduling bill due dates.

Phase 2: Get Liquid - Keep Money in Your Control

Stop locking money into 401(k)s and home equity. Chris argues the employer match doesn’t overcome the long-term performance drag - he cites underperformance of over 2% annually before fees in many funds. Instead, he builds reserves in high-yield savings accounts and whole life insurance (where he earns 6% tax-free). Target: 6 to 12 months of reserves for most people; 12 months for business owners and high-income earners.

Liquidity matters more than most people realize. According to Bankrate's emergency savings data showing only 46% of Americans can cover three months of expenses, and nearly one in four have no emergency savings at all - exactly why accessible reserves are the foundation of this entire framework.

Phase 3: Get Out - Invest for Cashflow, Not Appreciation

Once you have $150,000 to $200,000 in accessible capital, the goal shifts to generating alternative income streams. Chris’s rule: diversify across multiple vehicles that produce consistent cashflow each month, and never concentrate in a single asset.

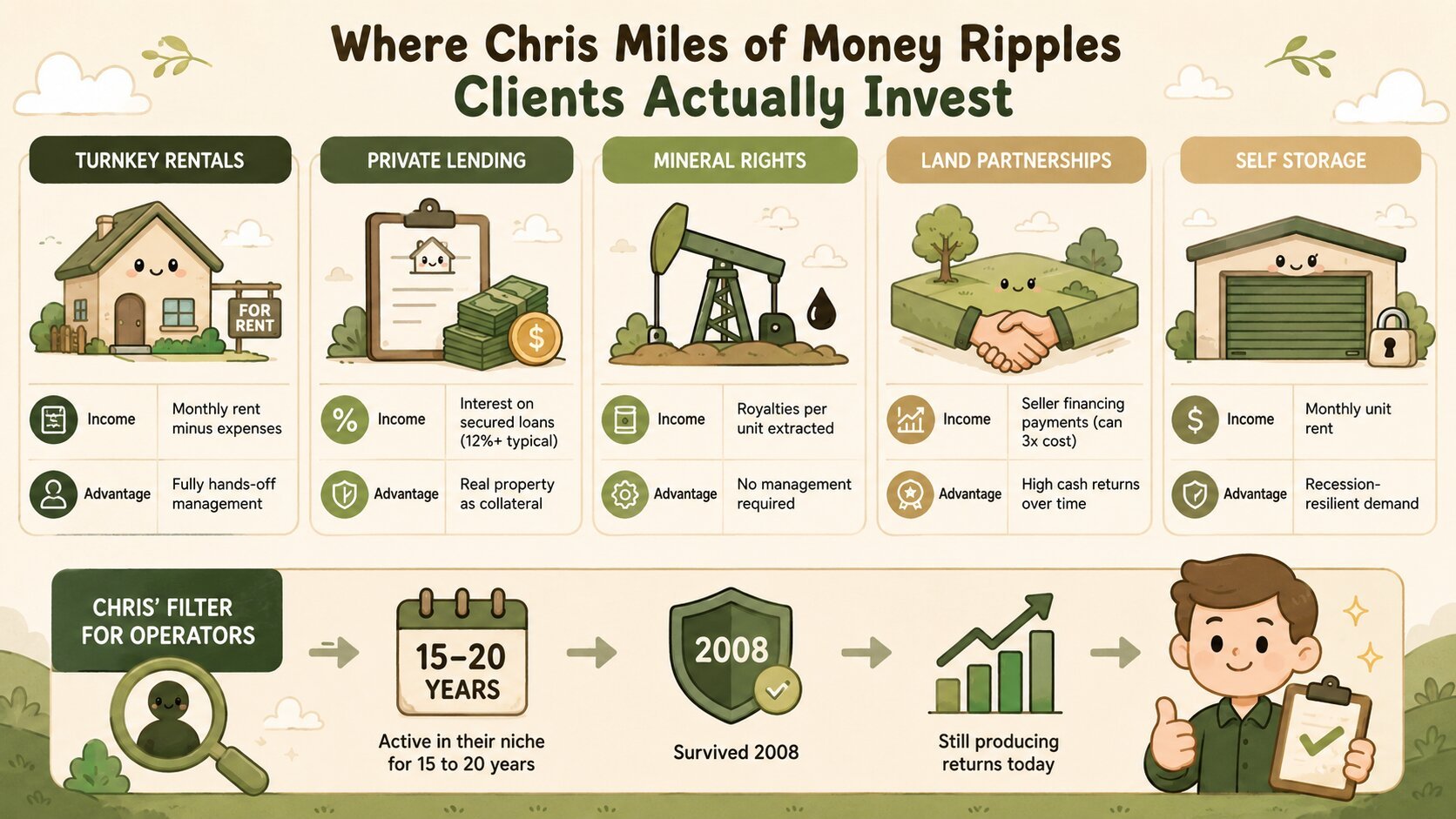

Where Chris Miles of Money Ripples Clients Actually Invest

Most financial content stays vague. Chris didn’t. Here are the vehicles he uses and what makes each one work:

|

Investment Type |

How It Generates Income |

Key Advantage |

|

Turnkey Rentals |

Monthly rent minus expenses |

Fully hands-off management |

|

Private Lending |

Interest on secured loans (12%+ typical) |

Real property as collateral |

|

Mineral Rights |

Royalties per unit extracted |

No management required |

|

Land Partnerships |

Seller financing payments (can 3x cost) |

High cash returns over time |

|

Self Storage |

Monthly unit rent |

Recession-resilient demand |

His filter for operators: experience through adversity. He doesn’t invest with people who started in 2018 or 2019. He looks for those active in their niche for 15 to 20 years - people who survived 2008 and are still producing returns today.

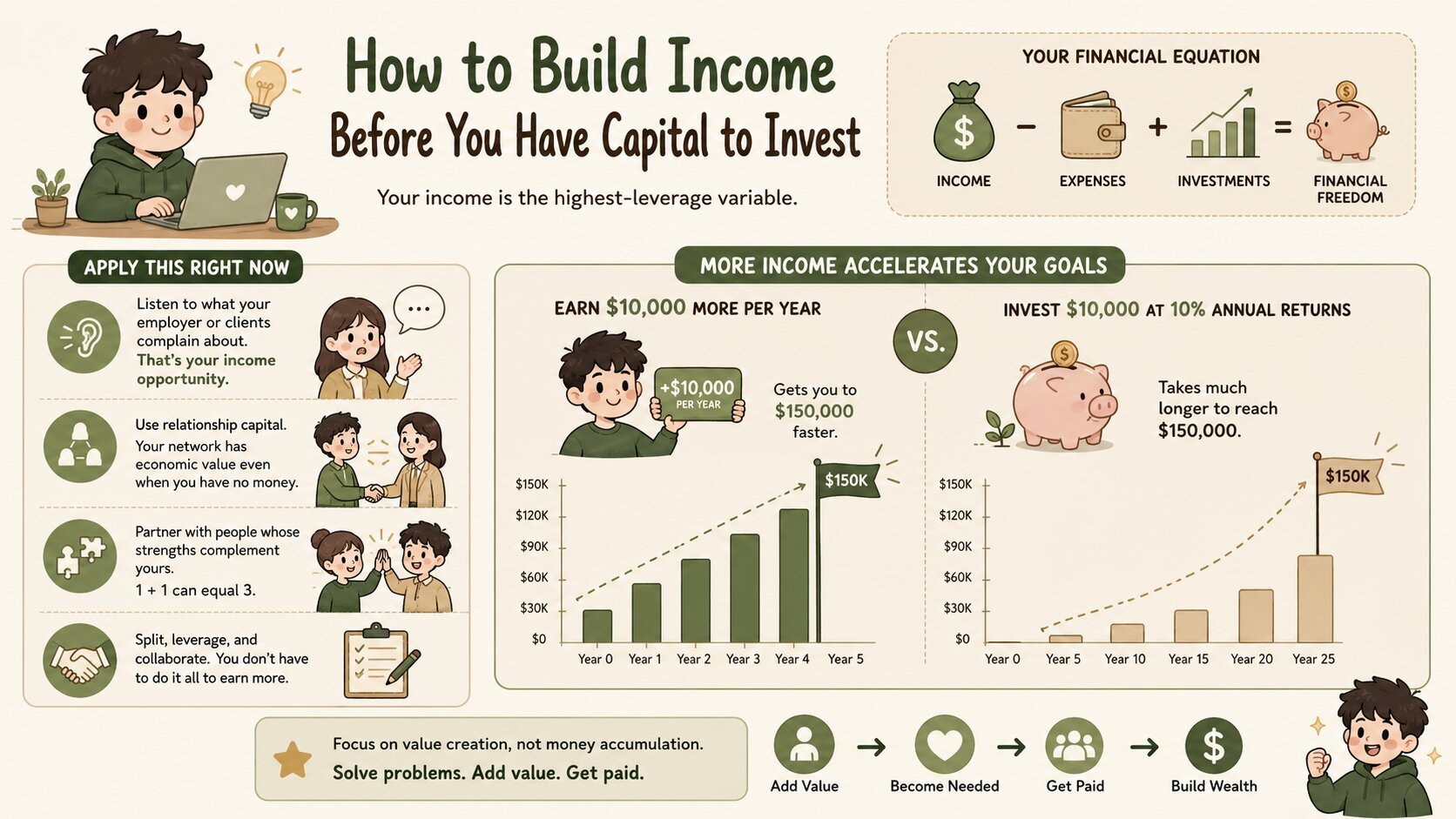

How to Build Income Before You Have Capital to Invest

Here’s what most financial content skips: what do you do when you don’t have $150,000 to deploy? Chris’s answer: income is the highest-leverage variable in your financial equation. You can only cut expenses so far - but there is no ceiling on what you can earn if you focus on value creation rather than money accumulation.

<blockquote> “Money is formulaic. Dollars follow value. The more value you can offer somebody - add value in such a way that they need you in their life - you will get paid money. I stopped asking ‘how do I make more money?’ because that’s been broken. People have done that for generations and stayed broke. I always ask: how can I add more value? How can I solve problems for somebody using my unique gifts, talents, and strengths?” - Chris Miles, Founder of Money Ripples </blockquote>

Some practical ways to apply this right now:

-

Listen to what your employer or clients complain about. That’s your income opportunity

-

Use relationship capital. Your network has economic value even when you have no money

-

Partner with people whose strengths complement yours. Chris split commissions with a colleague who loved paperwork; Chris handled the clients

-

A side hustle generating $10,000 more per year gets you to $150,000 faster than investing $10,000 at 10% annual returns

If this conversation prompted you to think about the financial foundation beneath your home, a smart first step is getting a free home valuation in Charlotte to understand where your equity actually stands. And if you’re looking at listings in Charlotte metro area, North Carolina, now is a good time to think about cashflow potential alongside appreciation.

Frequently Asked Questions

What is the Get Lean, Get Liquid, Get Out strategy?

It’s the three-phase framework Chris Miles outlines in his book The Work Optional Blueprint. Get Lean means tracking your spending weekly to find money leaks before trying to budget. Get Liquid means building 6–12 months of accessible reserves rather than locking money up in 401(k)s or home equity. Get Out means deploying that capital into cashflow-producing investments ideally once you have $150,000–$200,000 ready to invest.

Why does Chris Miles recommend against maxing out a 401(k)?

Chris argues that most 401(k) funds underperform the market by over 2% annually before fees, and fees themselves can run 0.75% or higher. Over time, even a 100% employer match may only make up for those losses, not create meaningful wealth. More importantly, the money is locked up and cannot be accessed without penalties during emergencies. He recommends keeping money accessible and investing it in assets you directly control.

How much money do I need to start cashflow investing?

Chris recommends building to $150,000–$200,000 before pursuing passive income investing. Below that threshold, a single setback in one investment can wipe out your progress. Building to that level first through income growth, expense tracking, and accessible savings gives you the cushion to invest in multiple vehicles and absorb setbacks.

Keep the Conversation Going

Want to stop trading time for money and start building income that works while you sleep? Reach out to Chris Miles:

🌐 Website → https://moneyripples.com/

📘 Facebook → https://www.facebook.com/chris.miles9177/

🔗 LinkedIn → https://www.linkedin.com/in/chriscmiles

If something in this episode made you think, question, or take a fresh look at your finances, don’t let it stop here. Follow me:

🌐Website → https://athomeinthecarolinas.com/

📷 Instagram → https://www.instagram.com/AtHomeintheCarolinas/

📘 Facebook → https://www.facebook.com/HomeintheCarolinas

Apply to Be a Guest on the Make Yourself at Home Podcast

The people who move this industry forward aren't waiting for the market to stabilize - they're out here solving problems, building systems, and helping others do the same. If that sounds like you, I'd love to have you on the show. Whether you work in lending, brokerage, investing, technology, or any corner of real estate, your insights belong in this conversation.