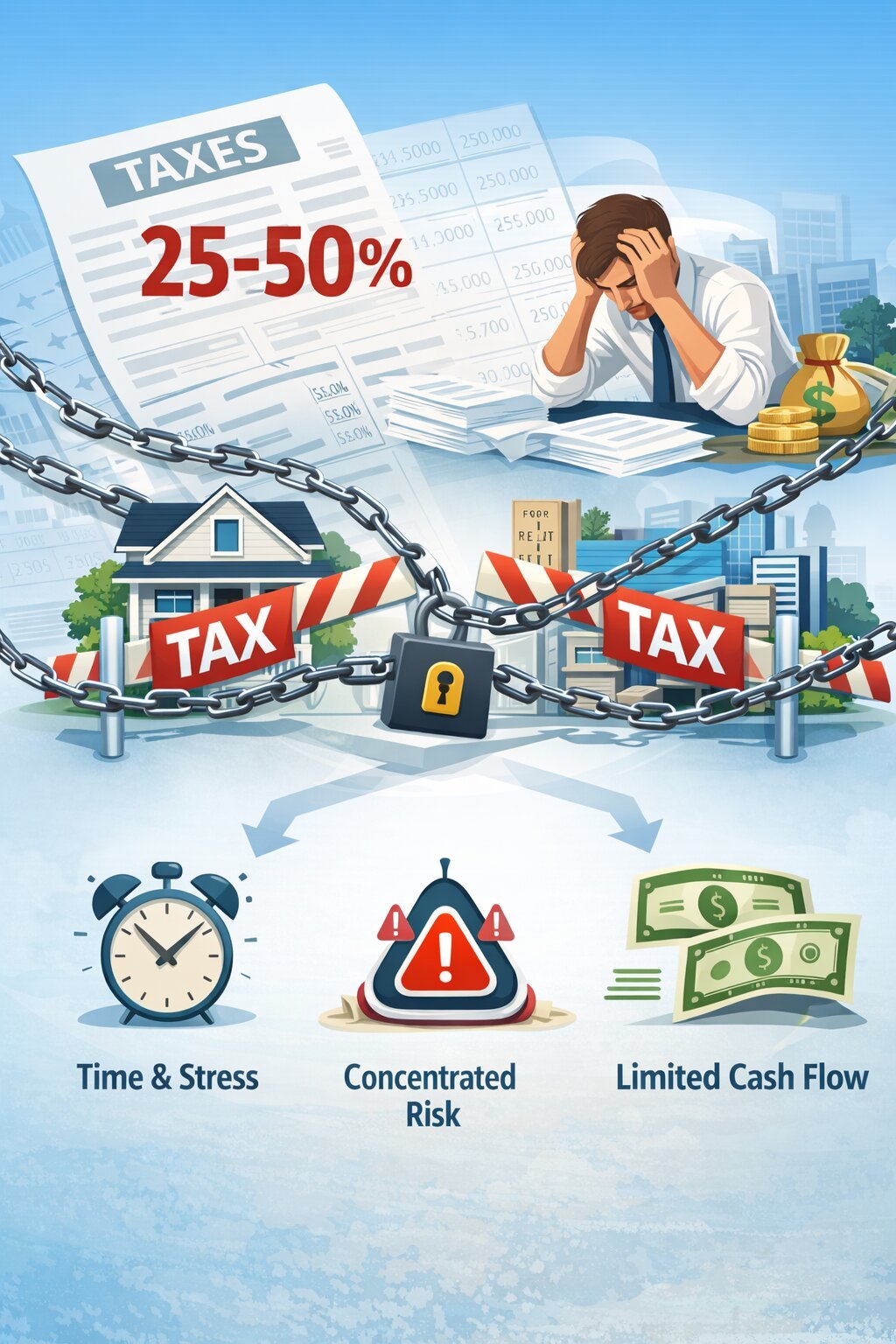

You've spent years - maybe decades - building equity in a property, a business, or a portfolio. And now that you're ready to sell, you're staring down a capital gains tax bill between 25% and 50% of your gains. The very thing you built to create freedom is now the thing keeping you stuck. Figuring out how to exit real estate without huge taxes, or how to defer capital gains tax on a business sale, can feel like an impossible puzzle - especially when the tools most people know about don't even apply to your situation.

That's exactly what I dug into on this episode of Make Yourself at Home. I sat down with Brett Swarts - founder of Capital Gains Tax Solutions and one of the country's leading Deferred Sales Trust experts - to break down a capital gains tax deferral strategy that solves this problem directly. Most real estate professionals have never heard of it. Most financial advisors don't bring it up. But if you're sitting on millions in unrealized gains, this conversation changes everything.

By the end of this article - and the full episode - you'll walk away knowing:

-

How the Deferred Sales Trust works, step by step

-

Why it outperforms a 1031 exchange in specific situations

-

How to create passive income after selling property

-

Real case studies showing exactly what's possible

And if you're ready to dig deeper into how the Deferred Sales Trust can help you defer capital gains and build truly passive income, here's the full conversation:

Who Is Brett Swarts & What Does Capital Gains Tax Solutions Do?

The Man Behind the Strategy

Brett Swarts is the Capital Gains Tax Solutions founder and host of the Capital Gains Tax Solutions Podcast.

His firm specializes in one thing: helping high-net-worth individuals legally exit highly appreciated assets without taking a massive tax hit.

His capital gains tax deferral strategy has been used by:

-

Investors

-

Business owners

-

Financial advisors

-

And families across the country.

And it works across a wider range of assets than most people realize.

What Assets Qualify?

If you're looking for alternatives to 1031 exchange (a tax strategy that lets you defer capital gains by reinvesting in like-kind real estate),

Or if you need a solution for assets that don't qualify for one at all, this strategy covers far more ground:

-

Primary homes

-

Commercial real estate

-

Business sales

-

Bitcoin exits

-

Stocks and collectibles

"We eliminate the need for the 1031 exchange. Our strategy, which is an installment sale with the trust, works with business sales, Bitcoin exits, primary home, commercial real estate, stock, collectibles - really any asset of any kind, as long as it has at least a million-dollar net proceeds and a million-dollar gain."– Brett Swarts, Capital Gains Tax Solutions Founder

The Minimum Requirement

To qualify, a seller needs at least $1 million in net proceeds and $1 million in capital gain.

These are multimillion-dollar exits - if you're in that range or approaching it, this strategy deserves serious attention.

The Catch-22: Why High Capital Gains Taxes Keep Investors Stuck

The Problem Most Sellers Face

Here's what I hear over and over - and I'm sure you've felt it too. You know it's time to sell. The asset has appreciated, the market is good, and logically it makes sense to exit.

But the moment you run the tax numbers, everything stalls. Whether you're trying to figure out how to defer capital gains tax on a long-held rental or how to exit real estate without huge taxes eating your gains, the path forward isn't obvious. As Brett mentions in our podcast:

"The biggest thing standing between you and truly passive income is typically the asset that you haven't sold yet, and the tax of which you would have to pay, of 25 to 50%. You've worked tirelessly to build your business or your real estate portfolio, but the thought of selling this brings more stress than relief because of the tax. That's part of the catch-22. I want to get out of it. I know I should get out of it. But if I do, I'm going to get crushed with tax."– Brett Swarts, Capital Gains Tax Solutions Founder

The Hidden Cost of Staying Stuck

However, holding onto an appreciated asset because of taxes carries its own costs:

-

Time and mental energy managing the property or business

-

Concentrated risk in a single asset, city, or market

-

Limited cash flow relative to total equity built up

-

No true financial freedom - even when you're 'wealthy on paper'

The good news: the Deferred Sales Trust is built specifically to break this cycle. Here's how it actually works.

What Is a Deferred Sales Trust (DST)?

The Basic Mechanics

A Deferred Sales Trust is an installment sale structure. You exit your asset, defer capital gains taxes, and receive income over time - without needing a 1031 exchange or any like-kind replacement. Here's the step-by-step process Brett walked me through:

|

Step |

What Happens |

Why It Matters |

|

1 |

Seller transfers asset to the DST |

Instead of selling directly to the buyer, the seller sells to an independent trust to begin the installment structure. |

|

2 |

DST issues promissory note to seller |

The note defines when payments start and how often they’re paid. The seller can choose immediate payments or delay up to 2 years. |

|

3 |

DST sells asset to end buyer |

The trust resells the asset at the same price, so it does not owe taxes on the transaction. |

|

4 |

DST invests proceeds |

Funds are invested inside the trust in a tax-deferred state, allowing growth before taxes are triggered. |

|

5 |

Seller receives installment payments |

The seller pays capital gains taxes only on the portion received each year. If structured properly, principal can remain fully deferred. |

Source: Capital Gains Tax Solutions, Deferred Sales Trust Strategy

"You're looking at having a trust set up that you're selling it to, and it's issuing you a promissory note, and this trust is selling it to the buyer. When you do it in this order and you have the buyer lined up to buy it from the trust, what happens is he's in a deferral state - meaning he only pays taxes as he receives payments back. He became the bank - the creditor to the trust."– Brett Swarts, Capital Gains Tax Solutions Founder

Why Investors Use a Deferred Sales Trust

-

Keep More Capital Invested

Instead of losing a large portion of your proceeds to immediate taxes, more of your money stays working inside the trust. More capital invested means:greater potential for growth, income generation, and long term compounding.

-

Control Your Tax Timing

You only pay taxes as you receive payments, rather than all in the year of sale. This helps manage tax brackets, reduce income spikes, and create more predictable financial planning.

-

Reduce Concentration Risk

You can sell a highly appreciated asset without triggering a massive upfront tax event. That makes it easier to diversify instead of staying overexposed to one property, business, or investment.

-

Design Your Own Income Stream

Payments can start immediately or be delayed, and can be structured as interest-only or installment payouts. This gives you flexibility to align income with retirement, lifestyle goals, or long term planning.

Why This Is Different From Everything Else

Brett was clear about what makes this strategy stand apart from other tax deferral approaches:

-

No 1031 exchange required

-

No charity required

-

No life insurance required

-

No gifting required

-

No like-kind replacement requirement

-

Works for primary residences - something a 1031 exchange simply cannot do

-

Has been in use for close to 30 years

Deferred Sales Trust vs 1031 Exchange

The Primary Home Gap

For anyone trying to figure out how to defer capital gains on primary home sales, the 1031 exchange is off the table entirely.

As highlighted by Investopedia, 1031 exchange was built only for investment or business properties - not primary homes. Primary homes don’t qualify unless you convert them.

That leaves most primary homeowners with limited options and no clean path to liquidity. The Deferred Sales Trust fills that gap directly, and it's a big part of why Brett built Capital Gains Tax Solutions.

"For the primary home, you're limited in the options for capital gains tax solutions. Most people know about the 1031 exchange - you can't do that with a primary home. But you can with our strategy. And that's part of why we started our company."– Brett Swarts, Capital Gains Tax Solutions Founder

Side-by-Side Comparison

|

Scenario |

Better Fit |

Why |

|

Selling a primary home |

Deferred Sales Trust |

1031 exchanges do not apply to primary residences. |

|

Want to buy a like-kind investment property |

1031 Exchange |

Designed specifically for reinvesting into similar real estate. |

|

Want diversification and passive cash flow |

Deferred Sales Trust |

Allows liquidity without forcing reinvestment into like-kind property. |

|

Selling a business, Bitcoin, or collectibles |

Deferred Sales Trust |

1031 exchanges only apply to real estate. |

|

Planning to hold until death for stepped-up basis |

1031 or Hold Strategy |

No sale means no capital gains triggered during lifetime. |

|

Multiple asset types or partners with different goals |

Deferred Sales Trust |

Flexible structure allows customized payout strategies. |

Case Study #1 - $8M Primary Home Sale (Tax Deferral + Cash Flow)

The Situation

This family in Palo Alto, California had raised six children in the property. The home had appreciated massively over the years, and with the kids grown and moved out, it was time to exit.

Knowing how to defer capital gains on primary home sales was critical here - as a primary residence, a 1031 exchange wasn't an option. The tax burden alone could have cost them hundreds of thousands, or stopped the sale entirely.

"We helped a seller of an eight-plus million dollar property in Palo Alto, California. It was their primary home. Six children - now all moved out of the house. The house had been a place of wealth for the family to grow, but also for capital to appreciate. We helped them exit the property, sell to a trust, defer the tax, pay off debt, diversify their wealth, and then get a passive cash flow coming in."– Brett Swarts, Capital Gains Tax Solutions Founder

The Result

By using the Deferred Sales Trust, the seller was able to achieve four goals at once:

-

Exit the property cleanly without triggering a massive tax event

-

Pay off existing debt

-

Diversify wealth across multiple asset types

-

Begin receiving consistent passive cash flow

That's the kind of outcome most sellers don't realize is possible - because most sellers don't know about the Deferred Sales Trust. And as this episode on the Make Yourself at Home Shorts shows, those outcomes are more achievable than people think.

Case Study #2 - $13M Commercial Exit (Car Wash Business)

From $500K to $13M - A Concentrated Position

Four partners bought land for about $500,000, developed it for roughly $3.5 million, and built a profitable car wash business.

By the time they were ready to exit, the business had grown to a $13 million sale. The capital gains tax on business sale of that size - with the gain concentrated in a single asset - could have been devastating without a plan.

"They bought this land for about $500,000. They developed it for about $3.5 million, and the value jumped from about $4 million all in to about $13 million. Three of the four partners had large multiple millions of dollars of gain and equity. They used this trust to defer their tax, diversify their wealth, and get passive cash flow coming in."– Brett Swarts, Capital Gains Tax Solutions Founder

Flexibility Across Partners

One partner had a smaller ownership stake and simply paid his taxes. The other three - each with multi-million dollar gains - each built their own trust structure, customized to their individual risk tolerance and cash flow needs. That flexibility is one of the Deferred Sales Trust's most important features: it works differently for every partner at the same table.

Case Study #3: Return on Time (ROT) vs Return on Investment (ROI)

A Different Way to Measure Wealth

Most financial conversations center on ROI - how much money your money makes. But Brett's Return on Time vs Return on Investment framework pushed back on this in a way that landed with me, especially for investors who've already built significant net worth.

Here’s the difference between ROI and ROT:

|

ROI (Return on Investment) |

ROT (Return on Time) |

|

|

What it measures |

Financial return on capital |

Time and freedom gained |

|

What it gives you |

More money |

More life |

|

Who prioritizes it |

Wealth builders in growth mode |

Wealth holders ready to exit |

|

The trade-off |

May require active involvement |

Requires letting go of control |

At the ROT stage of your life, the question shouldn’t be about how much you're earning. It should be about how much time you're getting back.

"ROT is return on time - what kind of time value are you getting out of these investments? If you've made your millions, or at least on paper you've made the millions, but you haven't been able to translate or convert your ROI to ROT - meaning you're going to get a better return on your time to free up your time and your energy and your stress - then what is the point of the ROI?"– Brett Swarts, Capital Gains Tax Solutions Founder

The Real Story Behind ROT

Brett shared a story about a client named Warren who owned a multi-million dollar property with significant gains. He had good property management in place - but he was still mentally on call.

-

Insurance doubled.

-

The bank had questions.

-

The manager needed managing.

-

His two young daughters were growing up while he was managing the manager.

After structuring the Deferred Sales Trust, Brett's team increased his cash-on-cash return - and Warren got all of his time back. That's the trade Brett describes as 'the three Ts for the two Ts': giving up the toilets, the trash, and the termites to get back time with his twin daughters.

Truly Passive Income - The Big Domino

Define the Number First

Before any investment strategy, tax plan, or exit structure, Brett says the most important thing is to identify your truly passive income number - the monthly amount that covers your lifestyle without trading your time for it.

Learning how to create passive income after selling property starts with knowing that number. That target is your north star. Everything else is secondary.

"We believe truly passive income is to your freedom and impact as compounding interest is to your money. It's not just about how to defer some tax or how to increase some cash flow - it's what amount of cash flow, if you didn't have to give up any more of your time, would be more than what you're making now. You're freeing up time on one end and increasing cash flow on the other. This creates transformational changes for families."– Brett Swarts, Capital Gains Tax Solutions Founder

The Path to Passive Income

"If you can get that big passive income number knocked over - 20, 30, 40, 50 thousand a month - then the rest of it either becomes irrelevant or it solves itself."– Brett Swarts, Capital Gains Tax Solutions Founder

Here's the path Brett outlines for how to build toward that number:

-

Identify the appreciated asset that's trapping your capital and time

-

Structure the Deferred Sales Trust before closing

-

Invest trust proceeds in cash-producing assets (Brett's clients typically see 8–12% cash-on-cash returns)

-

Receive consistent monthly deposits into your bank account

-

Use excess capital for further diversification, giving, or legacy building

Diversification After Exit - What Happens to the Money?

Total Flexibility, No Forced Reinvestment

One of the most common fears sellers have is: if I exit this asset, where does the money go?

-

With a 1031 exchange, you're forced into a like-kind replacement on a tight timeline.

-

With the Deferred Sales Trust, the answer is: wherever you want, on your terms.

Brett talks about it in detail in the podcast:

"Total flexibility, no like-kind replacement requirement. The investments can be made into securities, stocks, Bitcoin, other real estate - passive or active - other business ventures. That's really the important part to understand. When you're selling something, a lot of times real estate owners own it all in one property, or one city - it's all concentrated."– Brett Swarts, Capital Gains Tax Solutions Founder

Why Diversify in the First Place?

Most real estate investors arrive at the exit conversation with the same problem: everything is tied up in one asset, one market, or one city. That concentration worked during the growth phase but, according to Investopedia, it becomes a risk and a liability the moment you want liquidity, income, or flexibility.

Here's what concentration risk actually looks like in practice:

-

One property absorbs all your attention, time, and mental energy

-

One market downturn can wipe out years of appreciation

-

High-regulation, high-tax states like California, New York, and New Jersey add another layer of exposure

-

Cash flow stays thin relative to the equity you've built up

-

You have no ability to rebalance without triggering a massive tax event

The DST breaks all of that open at once. You exit the concentrated position, defer the tax, and redeploy into a mix of assets that actually matches where you are in life - not where you were when you bought in.

What a Diversified Allocation Can Look Like

|

Asset Class |

Example Within DST |

|

Passive real estate |

Syndications, real estate debt funds |

|

Equities |

Large-cap stocks, index funds, ETFs |

|

Alternatives |

Bitcoin, private equity, startups |

|

Income instruments |

Money market funds, bonds |

Brett's recommendation: start with what you know.

If real estate built your wealth, begin with passive real estate managed by best-in-class operators. Once your truly passive income number is secured, then branch out into other asset classes.

Market Cycles, Debt Flow & Tax Flow Strategy

Three Mindsets That Drive Smart Decisions

Beyond the DST itself, Brett shared a framework for how to read market cycles and position yourself ahead of them. It comes down to three simultaneous mindsets he calls:

-

Tax flow

-

Debt flow

-

Cash flow.

"When the trend is hyper-crushing the prices and things are a frenzy, I want to have a debt flow mindset that says I get out of debt. Why? Because I'm going to position myself to get debt later when the market is right for a buyer. You've got to have tax flow - because if I exit in the high frenzy, I've got to be able to defer the tax. And the most important is cash flow - what is your truly passive income?"– Brett Swarts, Capital Gains Tax Solutions Founder

Here are the three mindsets in detail:

|

Mindset |

What It Means Practically |

|---|---|

|

Debt Flow |

Reduce debt in hot markets; use smart leverage in buyer's markets |

|

Tax Flow |

Have a deferral plan ready before you exit at peak prices |

|

Cash Flow |

Know your passive income target and build toward it first |

What Brett Sees Right Now

In the episode, Brett shares his read on the current cycle. Residential real estate appears to be stabilizing and recovering, particularly in Q1–Q2 2026. Commercial - especially multifamily - still faces pressure from overleveraged deals. His advice: if you're not actively underwriting deals and making offers, you won't develop the pattern recognition to find real opportunities. The market rewards those who are in the game.

Who Benefits Most from a Deferred Sales Trust?

The Ideal Candidate

"Anyone who has a business, Bitcoin, real estate, or a primary home with multimillion dollar gains and are really looking for truly passive income - and they don't have it yet - those are the people who benefit the most."– Brett Swarts, Capital Gains Tax Solutions Founder

More specifically, this strategy is strongest for:

-

Business owners planning an exit with $1M+ in gains

-

Real estate investors in high-appreciation markets

-

Primary homeowners who don't qualify for a 1031

-

Baby boomers transitioning to retirement and seeking income

-

High-net-worth individuals who are asset-rich but time-poor

-

Partners in a business or property who each need customized plans

The Timing Question

For primary home sales, the trust must be in place before closing - there's no flexibility there. For commercial real estate, Brett's team can work through what they call the 'Best 1031 Exit Plan,' which uses an accommodator to create a short window after closing.

In some cases, a partial 1031 combined with a partial installment sale through the trust is the right answer. Either way, the earlier you bring Brett's team in, the more options you have.

When a 1031 Exchange May Be Better

Be Honest About What You Actually Want

Brett isn't trying to replace every tool in the box. He's clear about when a 1031 exchange is the right call - and that kind of straightforwardness is exactly what you want from a strategist.

"If you love the property and want to stay in the real estate game and buy another one, a 1031 exchange is less expensive. If you're going to hold until death and want a stepped-up basis, that can be a good strategy."– Brett Swarts, Capital Gains Tax Solutions Founder

A 1031 exchange has no trustee fees and no recurring management costs. If your goal is to keep buying and holding real estate in a like-kind rollover - and you genuinely love what you own - it's a simpler, more affordable option.

The Deferred Sales Trust is for when you want something different: liquidity, diversification, time, and income.

Generational Wealth & Stewardship

Beyond the Numbers

Throughout our conversation, Brett kept coming back to the 'why' behind all of this - what the money is actually for. A capital gains tax deferral strategy and a passive income number are tools. The real question is what you do with the freedom once you have it.

"Our company exists to unlock capital gains to multiply freedom and impact. It starts with their family — the freedom of time, the impact with the family. Then it really should move in a great flow: the flow of capital should move to hopefully giving and making a blessing to where God's called you to help others."– Brett Swarts, Capital Gains Tax Solutions Founder

Finance Your Life Mission

Brett frames it this way: use truly passive income to finance your life mission. Once your income number is covered, the capital you've unlocked becomes a tool - not just for your household, but for everything beyond it:

-

What breaks your heart?

-

What are you called to do?

-

What are you passionate about?

That's the question worth building toward.

Multi-generational wealth, at its core, isn't about money sitting in an account. It's about having the freedom to show up where it matters - for your family, your community, and the causes that need people with the resources to act.

Frequently Asked Questions

What Is a Deferred Sales Trust?

A Deferred Sales Trust is an installment sale structure where a seller transfers a highly appreciated asset to a trust, receives a promissory note, and pays capital gains taxes only as installment payments are received over time.

How Does a Deferred Sales Trust Defer Capital Gains Tax?

Instead of recognizing the full gain at the point of sale, the DST spreads it over time. You only recognize income - and owe taxes - as you receive installment payments from the trust. This is a legal, IRS-recognized installment sale method and one of the most effective alternatives to 1031 exchange for sellers who need flexibility.

Can You Use a Deferred Sales Trust for a Primary Home?

Yes - and this is one of its biggest advantages. Knowing how to defer capital gains on primary home sales is something most people don't realize is possible. The trust must be set up before closing on the sale.

What Is the Minimum Gain Required for a DST?

According to Brett Swarts, you need at least $1 million in net proceeds and $1 million in capital gain to qualify for the strategy.

Is a Deferred Sales Trust Better Than a 1031 Exchange?

It depends on your goals. A 1031 is simpler and less expensive if you want to stay in real estate with a like-kind property. The DST is better if you want liquidity, diversification, passive income, or are selling an asset that doesn't qualify for a 1031.

How Much Passive Income Can You Create After Selling Property?

This varies based on portfolio size and investment allocation. Understanding how to create passive income after selling property depends on how the trust proceeds are invested. Brett's clients typically see 8–12% cash-on-cash returns on trust-invested assets.

What Is Return on Time (ROT)?

Return on Time (ROT) is the value of reclaiming your time from actively managed assets. The Return on Time vs Return on Investment comparison is central to how Brett's clients evaluate their exits - freedom gained matters as much as financial returns.

Can You Invest in Stocks or Bitcoin Inside a DST?

Yes. Trust funds can be deployed into securities, stocks, Bitcoin, passive or active real estate, business ventures, or a diversified mix - with no like-kind requirement.

Who Qualifies for a Deferred Sales Trust?

Anyone with $1M+ in net proceeds and $1M+ in capital gain from a business, real estate, Bitcoin, primary home, stock, or collectibles. The strategy works across asset classes.

This podcast is produced by the Icons of Real Estate - #1 Real Estate Podcast Network

Apply to Be a Guest on the Make Yourself at Home Podcast

If you serve the real estate industry - through staffing, lending, brokerage, technology, or advisory - and help agents grow smarter, not harder… let's spotlight your insights.

Apply to be featured on the podcast.