Tax season is stressful enough without misinformation. Social media "experts" and outdated family advice can make it hard to know what's true and what might cause IRS trouble.

I sat down with my friend and CPA of 14 years, Branden Chopelas of Chopelas Tax and Small Business, to clear up the confusion. Branden Chopelas CPA North Carolina has over 20 years of experience guiding clients through the tax code and dispelling bad advice.

This conversation offers straightforward insights from a seasoned professional committed to accuracy.

About Branden Chopelas & Chopelas Tax and Small Business

Branden Chopelas is a North Carolina CPA with more than 26 years in the accounting field. She runs Chopelas Tax and Small Business, offering tax preparation in North Carolina, bookkeeping services NC, and small business accounting for clients across both North and South Carolina. Her firm also provides South Carolina tax preparation services for qualified clients.

Branden stands out with a compliance-first approach, ensuring clients remain legal and pay only what they owe.

"Even though I'm licensed in North Carolina, as long as I stay and work in North Carolina, I am eligible to work in any state in the United States on their tax return. I can't work in South Carolina and call myself a CPA, but I can work physically in North Carolina and do any tax return."

Her philosophy is simple: keep clients compliant and informed.

"Our job is to make sure that we keep you compliant with the tax law. We're trying to take advantage of the rules that we've been given to minimize your liability as much as possible. We're not out here to make you pay more in taxes."

For homeowners, real estate investors, and small business CPA North Carolina clients, that kind of clarity matters. It's the same clarity we aim for on the Make Yourself at Home podcast—pulling back the curtain on industries that affect your daily life.

Capital Gains on Selling Your Home — What's Actually True

Few tax topics create more confusion than capital gains tax on home sale questions. Every spring, homeowners have recurring questions, but Branden often reassures them that most will owe nothing.

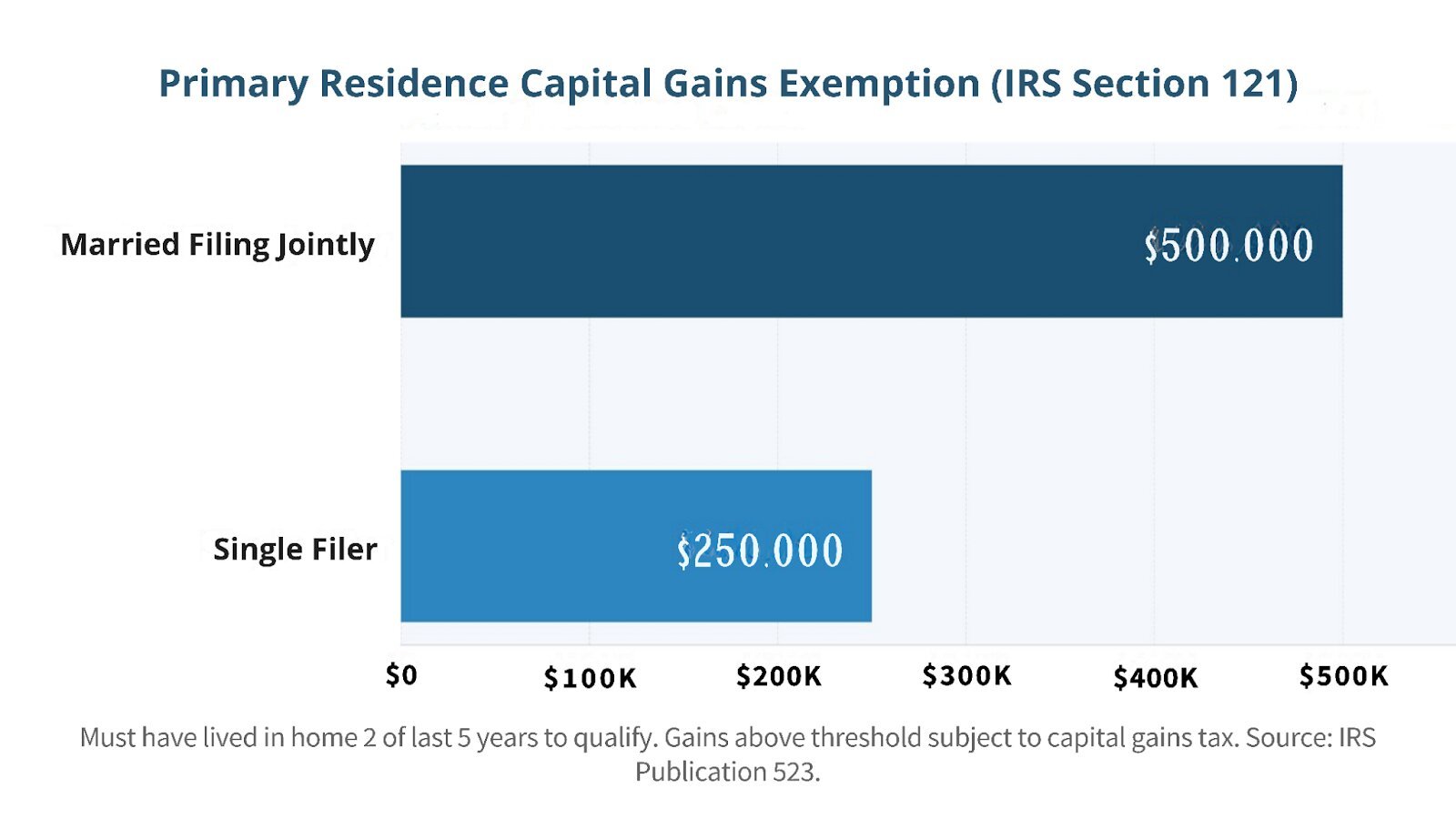

"If you have lived in your primary home for the last two of the five years, you can take up to $250,000 if you're single or $500,000 if you're married filing jointly as an exemption on the gain from selling your house. You can only take this exemption every two years."

Chart 1: Primary Residence Capital Gains Exemption (IRS Section 121)

For complete details, you can reference IRS official guidelines on primary residence sales. The IRS tax topic 701 page also explains these exclusion amounts clearly.

If you lived in your house for three years and rented it for two, you still qualify if you meet the two-year residency requirement. That 250000 500000 capital gains exemption explained simply means most homeowners won't pay a dime when they sell.

But here's where the old myths creep in. One of the most persistent pieces of bad advice? The idea that you can avoid capital gains by buying another house.

"That hasn't been around since the nineties. It doesn't matter if you take the profit from selling your house and put it into another house. It's still a taxable event. Just because you reinvest the money doesn't eliminate the tax."

Neglecting tax planning when selling a home can be costly, as it's a taxable event. Homeowners often wonder if major improvements like a new roof affect this tax.

Not exactly.

"HVAC, roof, windows—those are considered maintenance. You're maintaining the house in the condition you bought it in. But if you add onto the house or completely gut and renovate it and increase the value, that's different."

Are Home Improvements Tax Deductible When Selling?

Home improvements boost value if they surpass the original condition. A new roof prevents deterioration, and renovations can increase value and reduce taxes.

Understanding tax implications is essential before deciding the right time to sell. You can learn about how the real estate market is changing in the Charlotte Metro region to see how current conditions might affect your sale.

LLC Myths, TikTok Advice & Audit Traps

If you use social media, you've likely seen videos about secret tax strategies. Branden advises caution.

"If you see on TikTok 'the IRS doesn't want you to know this,' talk to a tax professional. The tax code for most people is pretty straightforward."

Much of the tax misinformation on TikTok leads people down dangerous paths.

One of the worst offenders? The idea that you can open an LLC to deduct personal expenses.

"You can open an LLC—that's relatively easy. But it has to be income-producing. It has to have a business purpose. There has to be a desire to make money. If you open it with no income and basic expenses, you are setting yourself up for an audit."

The truth about how LLCs are taxed is clearly laid out in IRS guidance on LLC taxation . The Treasury Department regulations also set ethical standards that tax professionals must follow.

The LLC tax write-offs myth persists because people want to believe there's an easy way to lower their tax bill. But opening an entity without a real business purpose is a recipe for disaster. The IRS sees right through it.

And audits aren't something to take lightly. The IRS has more reach than most people realize.

"Traditionally, they can only go back three years. But if they think you've been fraudulent longer, they can go back to the year you were born. It's not worth it."

When people ask the IRS about how far back they can go, the answer is sobering. The three-year rule corrects honest mistakes, but fraud has no time limit, leading to long-term consequences.

Tax Preparers, Refund Guarantees & Hidden Schedule C Risks

We all like the idea of a big refund. But if a tax preparer guarantees one, Branden says look closer.

"If you go to a tax preparer who guarantees a refund, make sure there is not a Schedule C or a Schedule E that you don't know about on your return. Because what they're doing is saying you have your own business and writing off expenses. That only sets you up for an audit."

The IRS audit techniques guide shows exactly what examiners look for on Schedule C returns. The IRS hobby loss rules explain when a business is considered a hobby for tax purposes.

Understanding Schedule C audit risk could save you major headaches down the road. Schedule C is for self-employment income. Schedule E rental income explained simply: it covers rental properties and partnerships. If you don't have either, those forms shouldn't be on your return.

Some preparers may add false income and expenses for a refund without your knowledge. While this may seem beneficial initially, it can lead to audit concerns later.

Here's the hard truth Branden wants every taxpayer to understand:

"You are 100% responsible for your tax return. If you sign it without looking at it, that's on you."

A tax preparer can make mistakes, but your name is on the return. Review the information, ask questions, and confirm your understanding. If it appears too good to be true, it likely is.

Comfort Letters & Why CPAs Push Back on Lenders

"Lenders ask for what we call a comfort letter. They want us to attest that everything in the tax return is 100% correct. We are not allowed to give that. To officially verify that information would require an audit that could cost no less than $5,000."

Understanding what is a comfort letter CPA means recognizing that CPAs prepare returns based on the information clients provide.

When clients ask why CPA refuses the lender letter, this is almost always the reason. CPAs can confirm they've prepared your return and showcase their experience, but legal restrictions limit their ability to provide the detailed "comfort letter" lenders need, causing hesitation.

Insider knowledge inspired the creation of our show. Real estate professionals aiming to share their expertise can join the Icons of Real Estate podcast network to connect with listeners who value transparency.

Hiring Your Kids in Your Business — What's Legal?

The strategy sounds genius: hire your children, pay them, and lower your taxable income. It works, right? Sometimes. But the rules around hiring your kids in your business are more specific than most people realize.

"If you're self-employed, you can hire your own kids. But you must pay them what you would pay someone else qualified to do that job. You cannot hire your child to sort email for $20,000 a year."

The IRS rules on children's income clarify what's required when employing family members. For deeper detail, IRS Publication 929 covers tax rules for children and dependents.

There is one modern exception Branden notes: content creators.

"If your children are part of your content and without them you couldn't make that income, that may be appropriate. But it's specific, and you need to talk to a tax professional."

Rich People Loopholes — Or Just Different Income Types?

Every few years, political candidates' tax returns ignite national debate about how the wealthy pay so little and whether a separate tax code exists for them.

No, Branden says. The rules are the same for everyone.

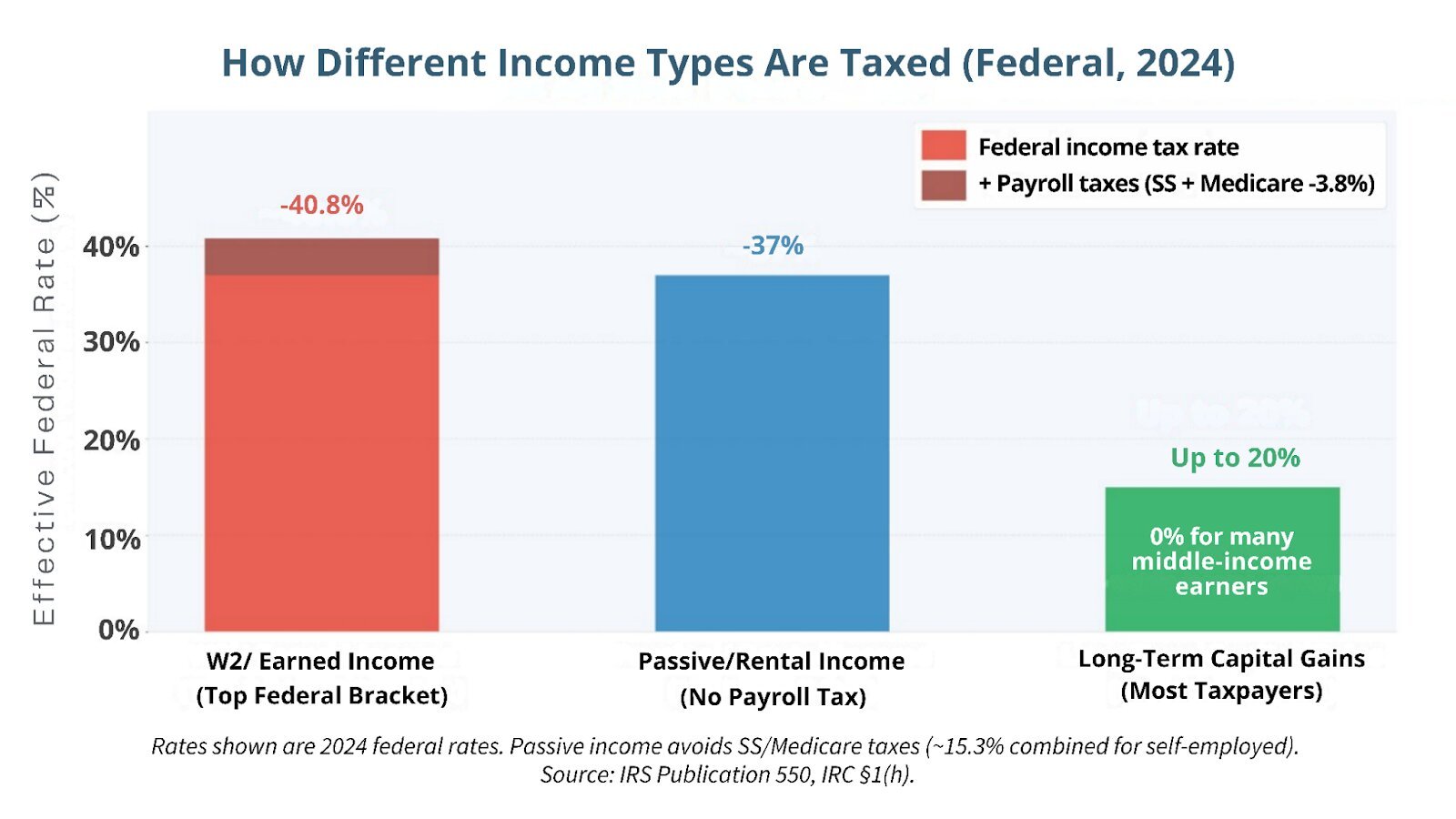

"The tax code is the same. The brackets are the same. The difference is diversification. Capital gains are capped at around 20%, while W2 income can be taxed much higher. Wealthy individuals often earn more through capital gains and passive income."

Chart 2: How Different Income Types Are Taxed, Federal 2024

The rich people's tax loopholes actually come down to how income is structured. The difference between passive income vs W2 taxes is substantial.

W2 income is taxed heavily, while rental and investment income bypasses payroll taxes and enjoys lower capital gains rates, aiding wealth growth through strategies like 1031 exchanges.

The lesson isn't about loopholes; it's about building diverse income streams. Real estate professionals can find success stories of agents who've done this through podcasting.

Preparing for Tax Season — W4 & Withholding Mistakes

An unexpected tax bill can ruin spring. Many are surprised each year to owe money, often due to a single box on a W4 form.

"The number one issue I see is married couples both working and not checking the box that says there's more than one income in the household. If you don't check that box, the IRS thinks your family is living on one income."

Use the IRS Tax Withholding Estimator to check if you're having the right amount taken from your paycheck. For detailed guidance, IRS Publication 505 covers tax withholding and estimated tax.

Learning how to adjust W4 for married couples can prevent that nasty April surprise. If both earn $75,000 but report only $75,000 total on W4s, you may owe taxes on the extra income.

The check box 2c W4 explained simply: it tells the IRS you have multiple earners in the household. The W4 update renders "claim zero" strategies useless. Update your W4 if you owe money. A quick check now can save thousands in April. HR can process changes anytime.

CPA vs EA vs Tax Preparer — What's the Difference?

Not all tax professionals are created equal. The difference between CPA and EA matters when you need representation.

"There's a tax preparer who prepares taxes but cannot represent you before the IRS. There's a CPA, like me, who can. And there's an EA, an enrolled agent, who has passed a difficult IRS test and can represent you as well."

For more on the credential requirements, visit the American Institute of CPAs or the National Association of Enrolled Agents.

Understanding tax preparer vs CPA vs enrolled agent helps you choose the right professional for your situation. A tax preparer can handle simple returns, but if the IRS questions you, you'll need a CPA or EA.

The CPA Shortage & Why Planning Matters

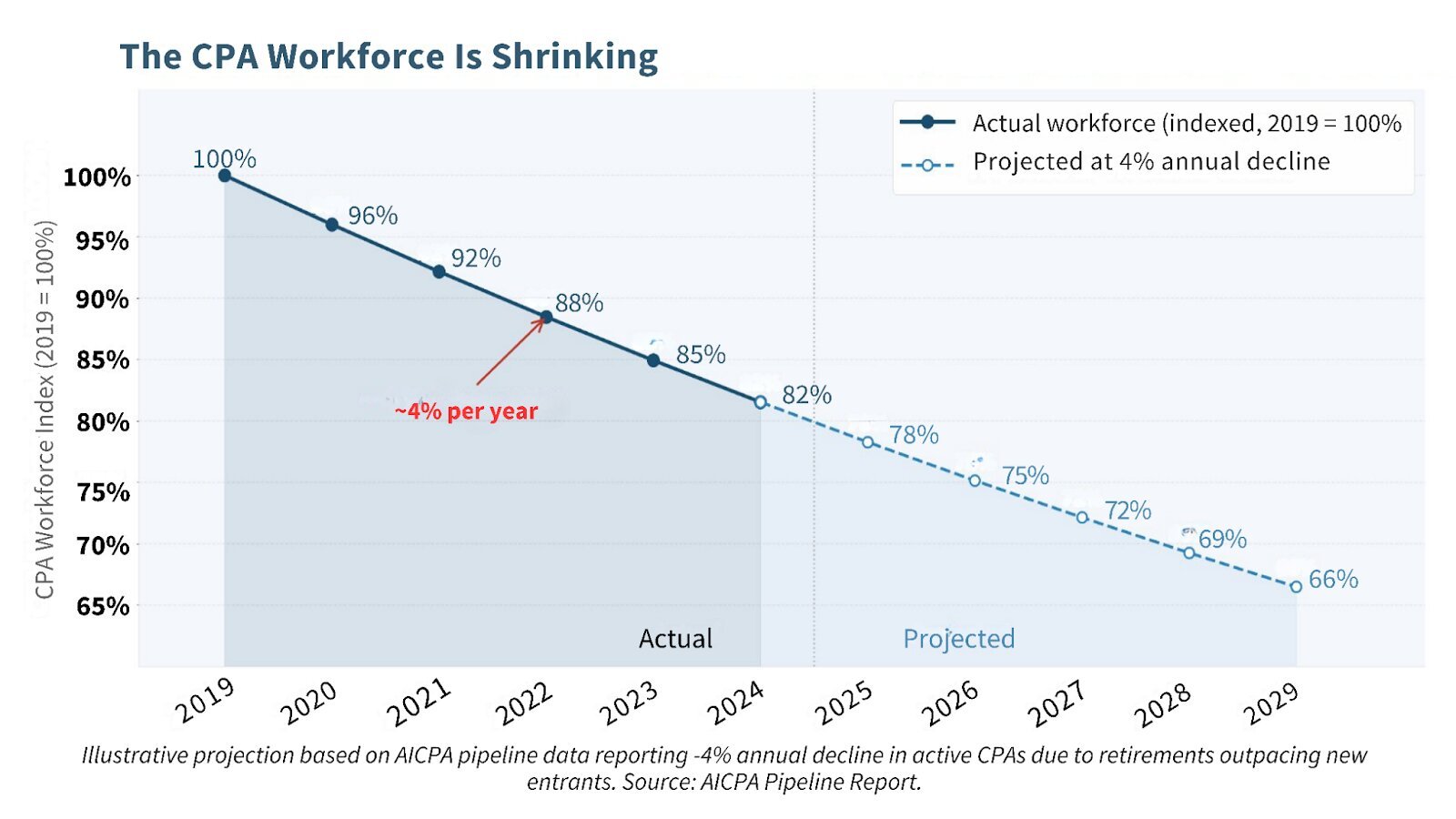

Here's something most taxpayers don't realize: CPAs are disappearing.

"We are dying out and retiring faster than we're bringing professionals in. That means higher fees and longer preparation times. It's becoming tighter and tighter."

Chart 3: CPA Workforce Decline Projected at ~4% Per Year

The profession is dropping 4% annually as accounting grads opt for higher-paying finance roles. Taxpayers should plan ahead.

Start early in finding a CPA and build relationships, as switching can be challenging. I provide the same kind of honest, upfront guidance that Branden offers her tax clients—cutting through the noise to help you make confident decisions.

This same principle applies to building your real estate business. Whether you're looking for guidance on launching your own podcast or wanting to explore other shows across the country , having the right team and tools makes all the difference.

Want to hear my entire conversation with Brandon Chopelas? Listen to our podcast episode!

FAQ

Do I have to pay capital gains when I sell my house?

Not if you've lived in it for two of the last five years and your profit falls under the $250,000 (single) or $500,000 (married) exemption.

Can I avoid capital gains by buying another home?

No. That rule ended in the 1990s. Selling triggers a taxable event regardless of what you do with the proceeds.

Are home improvements deductible when selling?

Improvements that increase your home's value can reduce your taxable gain. Routine maintenance does not.

Is opening an LLC a way to deduct personal expenses?

No. An LLC must have a business purpose and generate income. Using one to deduct personal expenses invites an audit.

How far back can the IRS audit me?

Typically three years. But if fraud is suspected, they can go back indefinitely.

What is a Schedule C, and why is it risky?

Schedule C reports self-employment income. If you don't actually have a business, having one on your return is fraud.

Why won't my CPA sign a comfort letter for my lender?

Because doing so would require an expensive audit. CPAs can't ethically guarantee 100% accuracy without one.

Can I hire my children in my business?

Yes, but you must pay them fair market value for actual work performed.

Are there special tax loopholes for rich people?

No. Wealthy individuals often earn more through capital gains and passive income, which are taxed at lower rates.

What's the difference between a CPA, EA, and a tax preparer?

CPAs and EAs can represent you before the IRS. Tax preparers generally cannot.

Why do I owe taxes every year even though I'm married, filing jointly?

Your W4 likely doesn't account for both incomes. Check the box indicating multiple earners.

Are moving expenses deductible in 2025?

Only for active-duty military members with qualifying moves. Current rules mean the moving expenses tax deduction for 2025 is extremely limited for most taxpayers.

Branden Chopelas offers over 20 years of tax expertise in a clear, accessible manner, aligning with Make Yourself at Home's mission of fostering meaningful conversations. He provides solutions for homeowners, small business owners, and W2 earners facing tax issues.

Connect with Branden and his team at Chopelas Tax and Small Business through chopelastax.com for support in maximizing your earnings.

Apply to Be a Guest on the Make Yourself at Home Podcast

Real estate is changing with shifting capital and tightening markets. If you're involved in construction, finance, brokerage, or development and addressing real issues, we want to hear from you.

Interested in sharing your expertise? You can apply to be a guest speaker and join conversations just like this one.

To dive deeper into podcasting, grab our free podcast framework guides covering everything from equipment to guest booking to marketing.

This podcast is produced by the Icons of Real Estate - #1 Real Estate Podcast Network.