Most people walk into the home-buying process believing it's straightforward: find a house, get a loan, and move in. But the financial reality is far more layered, and what buyers don't know going in can cost them tens of thousands of dollars.

I recently had the pleasure of sitting down with Kim Venable of Fairway of the Southeast, a mortgage consultant with over 30 years of experience helping families across the Carolinas and Florida achieve homeownership. Kim has worked alongside me at At Home in the Carolinas for years, and this conversation is exactly what I wish every buyer could hear before they start the process, whether you're just beginning to browse homes for sale or already under contract.

Here’s a preview of that episode:

Why I Had This Conversation

Financial literacy isn't taught in schools. Nobody sits young adults down and explains what a debt-to-income (DTI) ratio is, why mortgage insurance exists, or how the rate market actually functions. I see the fallout from those gaps regularly—confident buyers who freeze the moment the mortgage conversation starts.

Kim is one of the few professionals I refer without hesitation. She's experienced, direct, and she'll tell you what you need to hear, not just what sounds good. That's exactly why I brought her on.

Build a Real Budget Before You Build Expectations

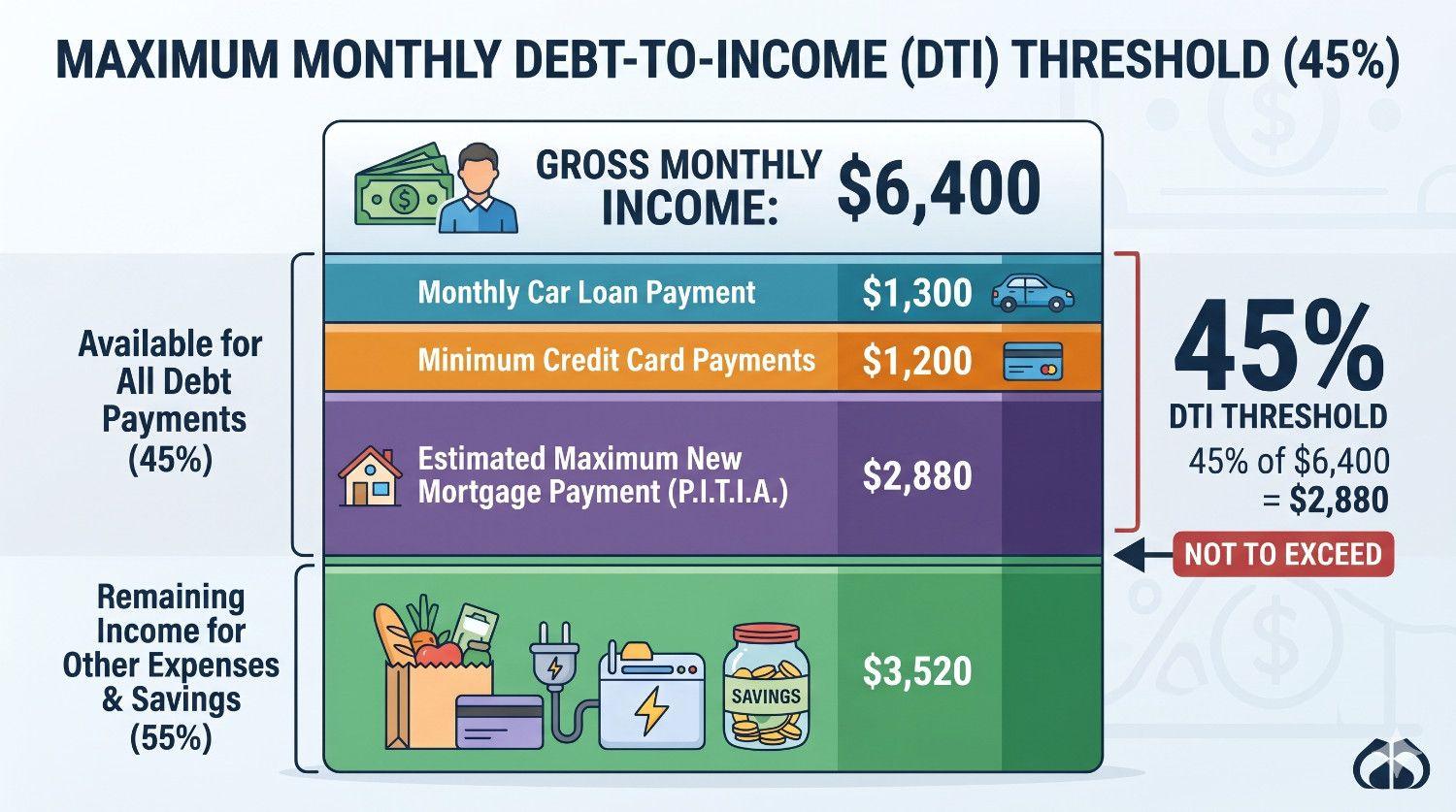

Kim's first and most important point is one most buyers skip entirely: know your numbers before you know your wish list. Most people think about what they want to spend, not what they can realistically afford after taxes, existing debt, and monthly obligations are factored in.

Her guideline is to take your gross monthly income and divide it by two. That number is your ceiling for all monthly debt payments combined—car loan, credit cards, and your new mortgage payment. Most loan programs require a DTI at or below 45%, and Kim recommends first-time buyers stay comfortably within that threshold.

If you bring home $6,400 a month, you want all monthly obligations under roughly $3,000. Run that number against a car payment, credit card minimums, and a mortgage, and the picture gets real fast. Budget is the foundation.

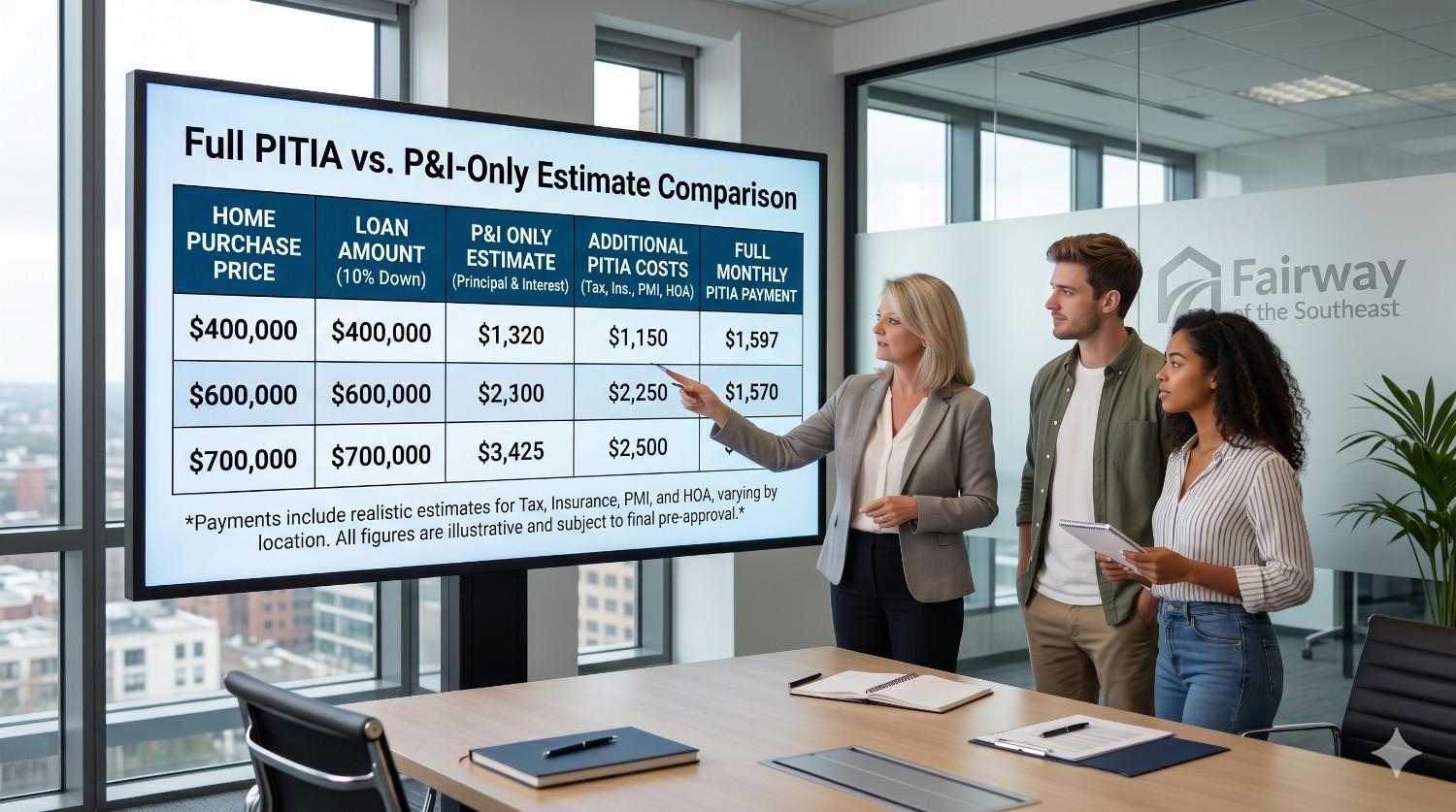

The Five Parts of a Mortgage Payment (And Why Online Calculators Mislead You)

The monthly payment estimate you find on a mortgage calculator is rarely the real number. What most tools display is only principal and interest, and that figure can be hundreds of dollars short of what you'll actually owe each month.

A complete mortgage payment includes principal, interest, property taxes, homeowners' insurance, and potentially private mortgage insurance (PMI) if you're putting less than 20% down. Some communities also carry HOA dues on top of all that.

Understanding these mortgage payment components before you start budgeting is essential, not optional.

"I want to keep building so that when they come, I can actually spend time with them. And when they get older, I want to give them something. Nobody was really able to give me anything except a headache. I love my parents and know they did their best, but with the resources I have, I want to create generational wealth — so my kids can pass things down, and their kids after that."–

Kim used a real example:

A $700,000 home with 10% down. Principal and interest alone landed at $3,700 a month. Layer in taxes, insurance, and PMI, and the real number climbs significantly. The 20% down myth persists, but with strong credit, PMI is often far less costly than buyers assume, and in many cases, putting less down and keeping the rest invested is the smarter financial move.

Why Pre-Approval Comes Before Everything Else

I've seen it happen too many times. A buyer falls in love with a home, writes an offer, and then finds out they don't qualify. It's avoidable, every single time, with one step: get pre-approved before you start looking.

Pre-approval means a lender has reviewed your actual income documents and credit history, the same way an underwriter will. It gives you real buying power, not a number based on what you told someone over the phone.

Key mortgage pre-approval tips from Kim: don't open new credit accounts, don't close existing ones, don't change jobs without your lender's clearance, and document any unusual deposits right away.

"Try to keep your credit the same from the time you talk to a lender until the time you close," she told me. "The more we know, the easier it is to help."

Any of these missteps can stall or derail a closing that's days away. The process protects you, but only if you follow it.

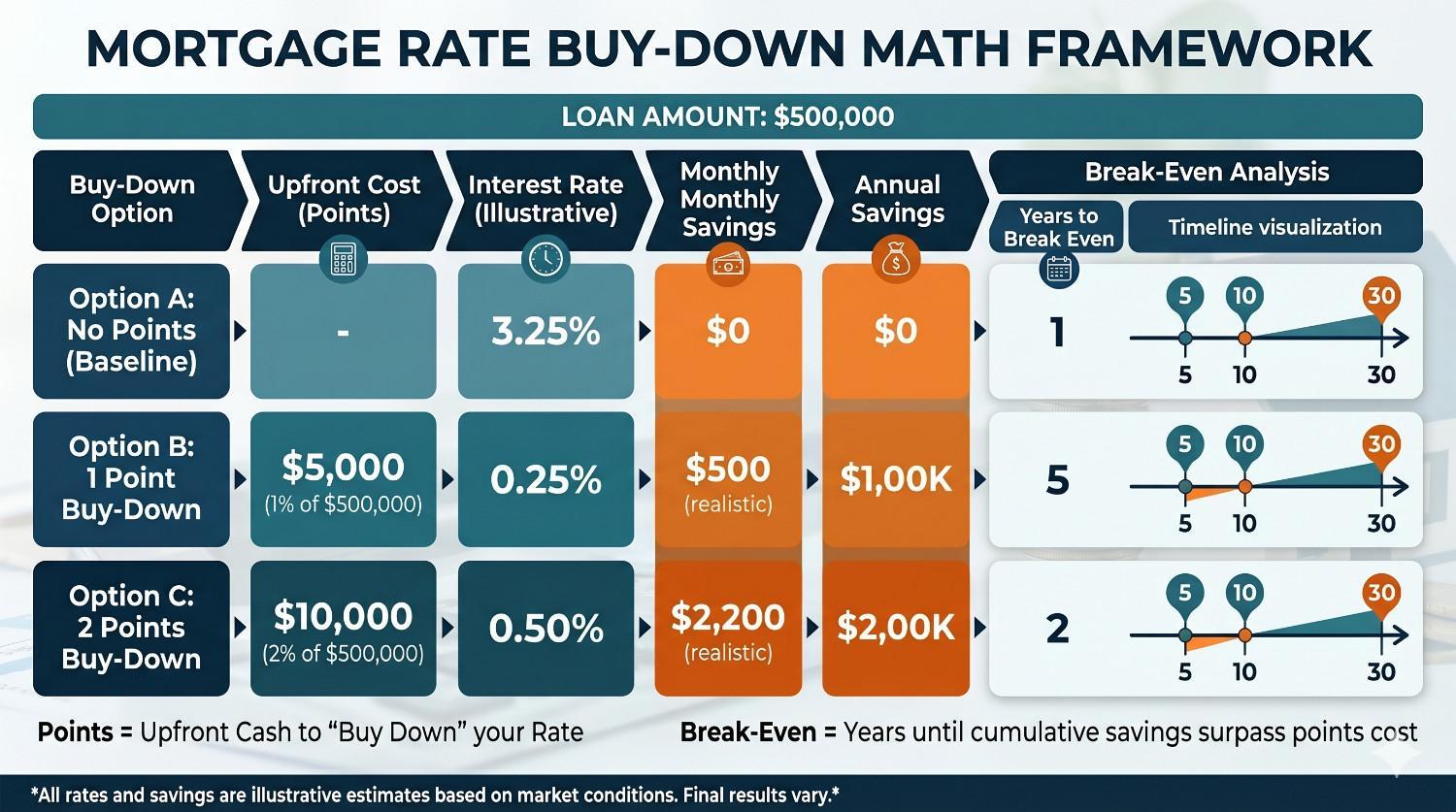

Interest Rates, Points, and How the Mortgage Market Really Works

Here's what surprises almost every buyer Kim talks to: you can have any interest rate you want. That's not a marketing line—it's literally how the mortgage market functions.

Kim walked me through a live rate grid during our conversation, pulling directly from Fannie Mae and Freddie Mac. Multiple rates are available every single day. A rate near market carries little to no upfront cost. A significantly lower rate can cost $15,000 to $28,000 in points.

Mortgage points explained simply: one point equals 1% of your loan amount. On a $500,000 loan, one point is $5,000. Four points to chase a lower rate? That's $20,000 before you've unpacked a single box.

"When my clients send me estimates showing 4% or 4.5% rates, I look at those loan estimates carefully. They may be getting that rate, but they're paying $28,000 for it. That is not a good deal. I ask every client: how long are you going to be in this house, and how much does that lower rate actually save you?"–

Rates also move daily, sometimes two or three times within a single day. Unless you're comparing the same product, the same loan amount, and the same credit profile at the same moment, those online rate comparisons are unreliable.

And historical context matters: rates in the low sixes are historically normal. The 3% era required a global pandemic. We shouldn't want to go back.

What Changed for Me After This Conversation

"It takes a team to get a client from beginning to end. And it takes experience. Anybody can say, 'Sure, I can get you a loan.' But are you being educated through the process? That's what I'm seeing—and that's what matters most."–

That's the line I keep coming back to. As your real estate agent, I can walk you through every showing, negotiate on your behalf, and protect your interests at the table. But I cannot walk you through a rate grid or explain why one loan product fits your situation better than another. That's Kim's job, and it requires someone with both the knowledge and the willingness to pick up the phone.

What this conversation reinforced is that the right homebuying team lender-realtor combination changes your entire experience. The best lender isn't necessarily the one with the lowest advertised rate, but one who explains the full picture, tells you the truth, and stays accessible throughout the process.

If you're ready to explore your options, you can review available mortgage loan products before your first showing. And when it's time to search, Kim Venable of Fairway of the Southeast and the right team will be in your corner from day one.

Want to hear my full conversation with Kim on avoiding mortgage rate traps and buying smart?

Frequently Asked Questions

How do I know if I can afford the home I want?

Start with your gross monthly income and divide it by two. That's your ceiling for all monthly debt payments combined. Subtract existing obligations to see what's realistically left for a mortgage. A lender can confirm the real numbers with a proper pre-approval review.

Do I really need to put 20% down to buy a home?

No, and this is one of the most persistent myths in home-buying. Programs are available with as little as 3% to 5% down. With strong credit scores, PMI can be a minimal monthly cost, and in many cases, investing your remaining capital rather than depleting savings for a larger down payment makes better long-term financial sense.

What should I avoid doing between pre-approval and closing?

Don't open any new credit accounts, close existing ones, change jobs without lender clearance, or make large unexplained deposits. Any of these can trigger a re-review by underwriting and delay (or kill) your closing. When in doubt, call your lender first and get clearance before taking any financial action.

Apply as a Guest on the At Home in the Carolinas Podcast

Real estate and mortgage markets shift constantly, and buyers deserve access to the professionals who live and work in this industry every day. If you're an expert in lending, real estate, insurance, or any part of the home-buying process, and you're ready to share what you know, I'd love to have you on my show!

Make Yourself at Home is produced by Icons of Real Estate, the #1 Real Estate Podcast Network. If you are a real estate professional, apply to be a guest speaker across the network!