For 18 years, I said the same thing to every buyer I sat down with: “Once your credit gets pulled, your phone is going to blow up.” That was not a warning I wanted to give. But it was the truth, and my clients deserved to be prepared.

Hundreds of calls, texts, and emails flooding in the moment they applied for a mortgage. Some from people pretending to be affiliated with their actual lender. Some targeting first-time buyers who had no idea what was happening or why. And I had no real answer for them beyond: “Just ignore it. It’ll stop eventually.”

So when I heard that Brendan McKay of McKay Mortgage Broker Action Coalition - had spent three years pushing federal legislation to stop it, I knew I had to get him on the Make Yourself at Home podcast. This episode is that conversation.

Here is what you will walk away knowing:

-

What trigger leads actually are and who was responsible

-

What the Home Buyer’s Privacy Protection Act changes - in plain language

-

What three years of federal advocacy taught Brendan about building a business on the right side of an argument

And more…

Or listen to the full conversation here.

Brendan McKay of McKay Mortgage Broker Action Coalition: What are Trigger Leads?

The mechanics of this problem are simpler than most people realize - and that’s part of what makes the whole thing so frustrating. As Brendan explained in the episode, the moment a mortgage company pulls your credit, the three major credit bureaus - Experian, TransUnion, and Equifax - sell your information to competing solicitors. A credit pull signals you are actively in the market for a mortgage. That data is valuable, and until recently, it was completely legal to sell it without your consent.

Here is the piece most people miss: the credit bureaus, which most consumers assume are government institutions, are publicly traded, for-profit companies. Selling trigger lead data was a revenue stream. Full stop.

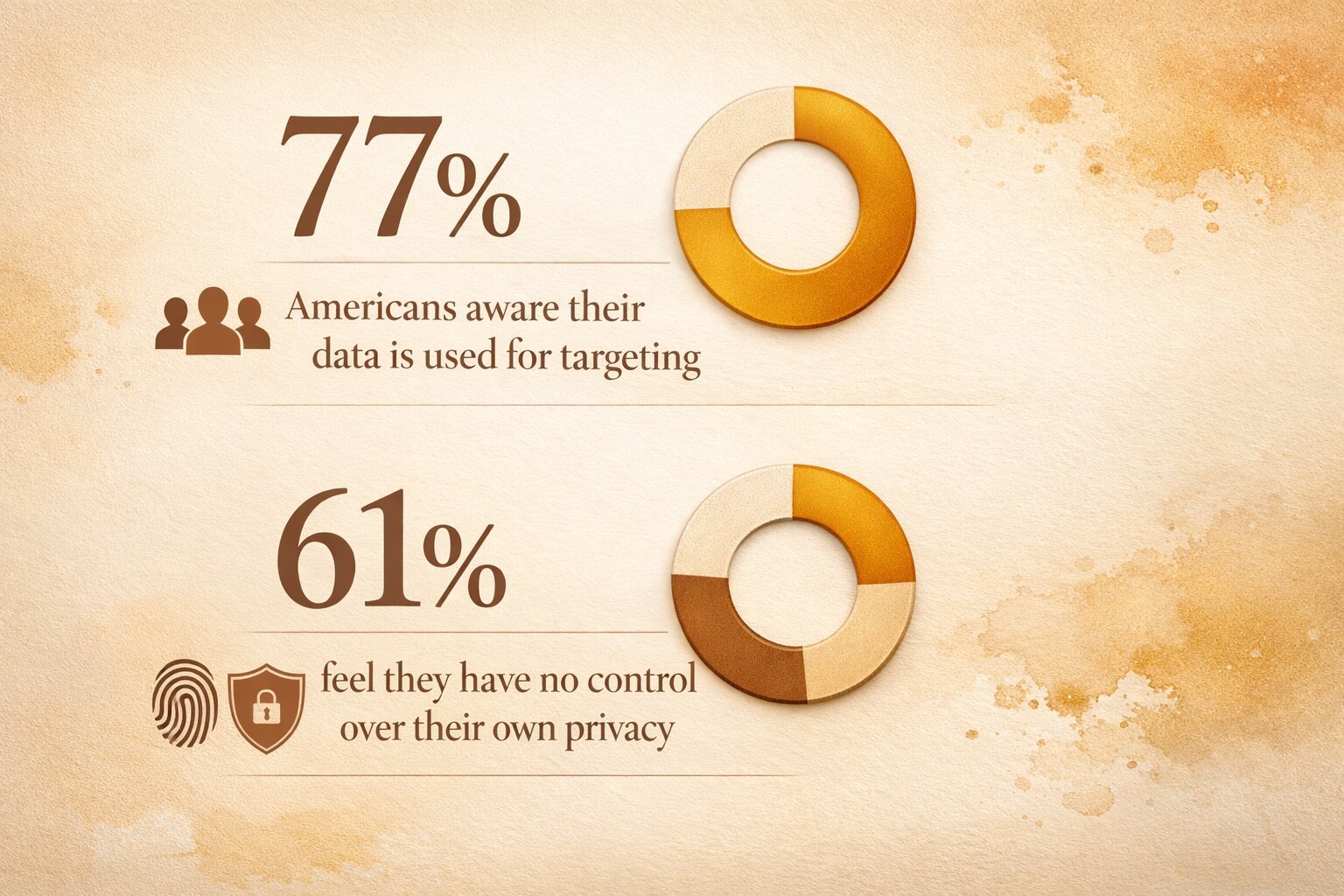

Most people already have a gut feeling that their data isn't safe. According to a Pew Research survey, 77% of Americans are aware that companies use their personal data for targeting and risk assessment. And a SAS-sponsored Futurum Research report 61% feel they have no control over protecting their own privacy.

That distrust was already simmering before anyone applied for a mortgage. So when a client’s phone starts ringing the moment their loan officer pulls credit, the natural assumption is that the loan officer sold their data. That destroyed trust - trust that took weeks to build - right at the most critical and stressful moment of a home purchase.

And for first-time buyers, ESL buyers, or first-generation buyers, the situation was even worse. Brendan told me on the podcast that solicitors would call and imply affiliation with the borrower’s actual lender - without technically lying. Vulnerable buyers would engage, get confused, and sometimes end up mid-process with someone completely different from the professional they had chosen and trusted.

“It just gets what’s already a complicated, stressful process off to a terrible start.”– Brendan McKay, Co-Founder and Chief Advocacy Officer of the Broker Action Coalition (BAC)

Understanding why this was happening is the first step. The next step is knowing what finally changed.

What the Home Buyer’s Privacy Protection Act Changes

The Home Buyer Privacy Protection Act trigger lead bill does one central thing: it requires your explicit opt-in before credit bureaus can sell your mortgage data to solicitors. Before the law, they did not need your permission. Now they do.

There are two narrow exceptions: the company currently servicing your mortgage, and the company that originated your last mortgage, can still use trigger lead data. Everyone else needs your consent.

Here is what that looks like in practice:

|

Before the Law |

After the Law |

|

Hundreds of unsolicited calls after credit pull |

Zero to two calls expected for most buyers |

|

No consumer consent required |

Opt-in required for data to be sold |

|

Trust erosion between buyer and loan officer |

Cleaner, clearer professional relationships |

|

First-time buyers vulnerable to deceptive solicitation |

Significantly reduced exposure |

“We are taking hundreds and thousands of phone calls and making it one or two. And if you are a first-time home buyer, you can probably expect to get zero.”– Brendan McKay, Co-Founder and Chief Advocacy Officer of the Broker Action Coalition

This bill passed unanimously - every single member of Congress voted yes, bipartisan, in both chambers. As Brendan pointed out, standalone bills almost never pass that way. Housing, he reminded me, cuts through partisan noise when someone does the work to explain the problem clearly.

Now let’s talk about what you can do with this information, starting with the mortgage process itself.

How to Shop for a Mortgage - Brendan’s Practical Breakdown

This is the section I wish I could hand to every client before their first lender conversation. I give my clients a list of lenders to call and a list of questions to ask - and after this episode, I updated that list.

According to a recent CFPB study, almost half of all borrowers seriously consider only a single lender or broker before deciding where to apply.

That is a costly mistake. Here is how to do it right, based on what Brendan laid out in the podcast:

-

Get quotes from multiple lenders. Do it within a two-week window so all the credit pulls count as one inquiry.

-

Compare only two variables: interest rate and lender fees. Title insurance and escrow estimates are either federally regulated or nearly identical regardless of lender - do not use them to compare.

-

Do not let rate alone guide you. A 6% rate with no lender fees can be a better deal than 5.75% with 1% in points. On a $400,000 home, 1% in lender fees is $4,000 out of your pocket.

-

Get everything in writing. If a lender gives you a better rate verbally, that number means nothing without documentation.

If a loan officer pushes back when you mention shopping around, walk away. That defensiveness is a red flag, not a negotiation tactic.

On the question of local vs. national lenders, Brendan made a point I completely agree with: local loan officers have skin in the game.

“If I start developing a reputation as somebody that does not close on time, that is a massive problem for me. If I am sitting in some call center half the country away, that same level of accountability simply does not exist.”– Brendan McKay, Co-Founder and Chief Advocacy Officer of the Broker Action Coalition

Local agents in a market know which lenders close on time and which do not. That reputation is a real performance incentive. Especially if you are buying - not refinancing - consider making local the default.

Understanding how to evaluate lenders connects directly to a bigger misunderstanding that Brendan addressed head-on: what a mortgage broker actually is, and how they fit into the process.

What Most People Get Wrong About Mortgage Brokers

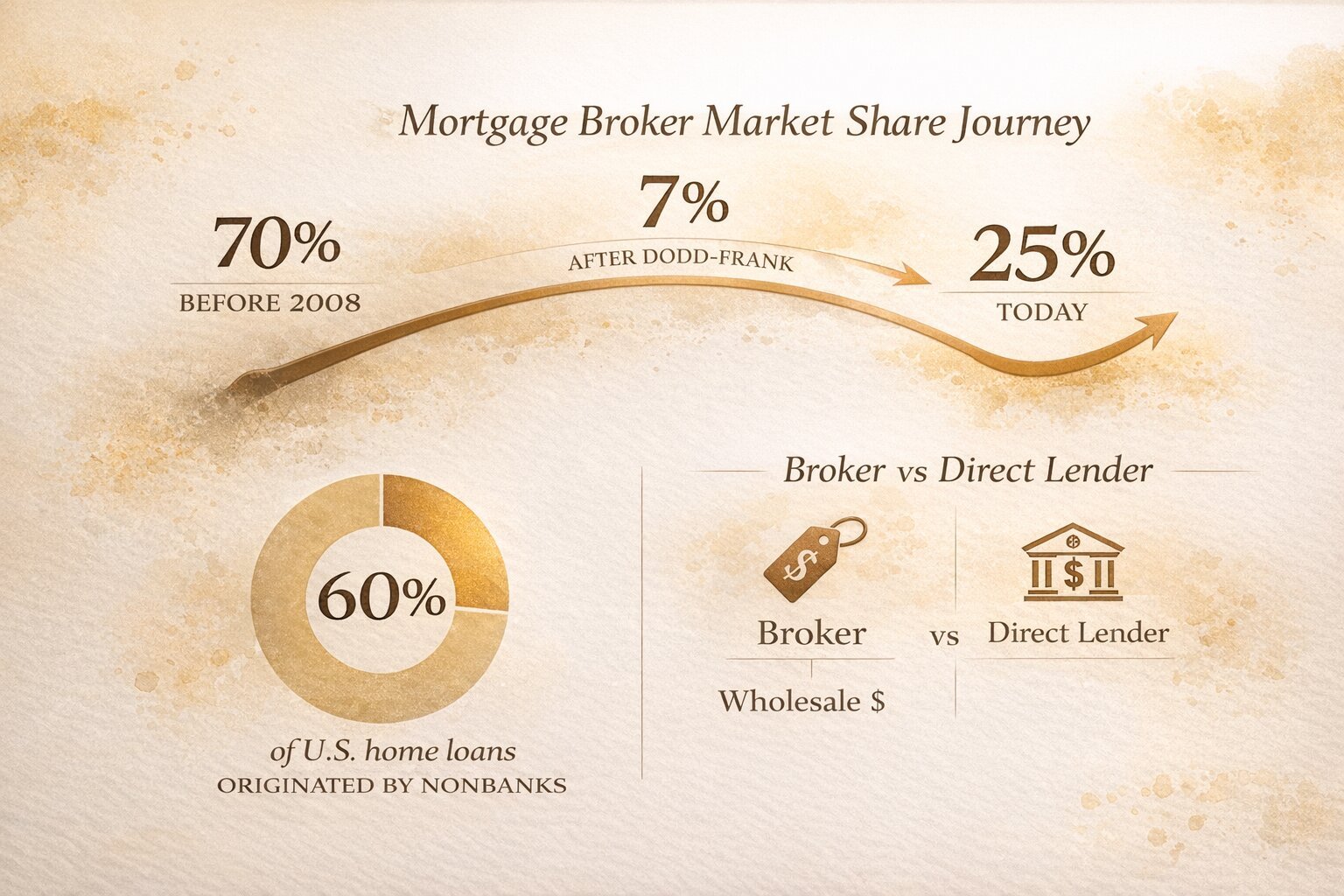

Before 2008, mortgage brokers originated about 70% of loans in the U.S. After the financial crisis and the passage of Dodd-Frank, that number dropped to roughly 7%. The industry rebuilt, and brokers now hold about 25% of the market again. But the old reputation lingered.

According to Bloomberg, nonbanks have dominated U.S. home loan origination in recent years, accounting for roughly 60% of all mortgages and pulling in approximately $71 billion in fees - nearly three-quarters of the total revenue collected across lenders and brokers.

The biggest misconception, as Brendan explained in the episode, is that a broker adds cost to the transaction. The reality works like any wholesale-to-retail model: the same lenders who sell loans directly to consumers also offer wholesale pricing to brokers - at lower rates. A well-run brokerage can often beat the pricing of a direct lender, even accounting for the broker’s compensation.

The mortgage broker vs direct lender comparison is not about which is cheaper by default - it is about accountability, access to products, and how that professional runs their business. Brendan’s advice on the podcast applies equally to both: shop, compare in writing, and watch for pressure tactics.

Knowing who you’re working with matters whether you’re looking for your first home or pulling up listings in the Carolinas. The mortgage relationship is as important as the property itself.

This brings us to something Brendan said that stayed with me long after we wrapped the episode.

What Three Years of Federal Advocacy Taught Brendan McKay - and What It Taught Me

Brendan took over 200 meetings with congressional offices over the course of this campaign. His approach in those meetings was the same approach he uses with first-time buyers: start at a low baseline, explain clearly, and bring solutions.

“I went into it never expecting it to be easy, but I continued on knowing that we were clearly on the right side of this argument. And as long as we were persistent, it was a matter of when, not if. Passing federal legislation is hard - and it should be hard. Three years sounds like a long time, and it is to you and me. But that is Lightspeed on Capitol Hill.”– Brendan McKay, Co-Founder and Chief Advocacy Officer of the Broker Action Coalition

He also talked about celebrating every incremental win - every co-sponsor added, every committee vote, every step forward. Not because they were the finish line, but because the process deserved recognition.

I took that directly back into my own thinking. Here are the lessons I pulled from our conversation that apply straight to real estate and mortgage work:

-

Start at a low baseline. Whether you are explaining a mortgage to a first-time buyer or explaining trigger leads to a member of Congress, assume nothing. Meet people where they are.

-

Bring solutions, not just problems. Congressional offices are full of people bringing problems. The professionals who get traction bring answers alongside them.

-

Being on the right side of an argument still matters. Money gets you access in DC, but a clean, consumer-first argument outlasts a well-funded opposition.

Small wins compound. Every milestone worth celebrating is worth making a big deal of. It builds momentum and morale at the same time.

The breakthrough moment for Brendan was sitting in the gallery of the House floor, without his phone, watching the vote happen in real time. He went and sat on the steps of the Capitol for an hour and a half afterward. That is the kind of moment you earn with three years of persistence.

If you want to understand what changed for home buyers here in Charlotte and the Carolinas - whether you’re looking at a home valuation in Charlotte or browsing available properties - this conversation is worth your time from start to finish.

Keep the Conversation Going

If you have mortgage questions or want to learn more about Brendan's advocacy work, reach out to him directly.

Follow Brendan McKay:

LinkedIn → https://www.linkedin.com/in/brendan-mckay-5473649

Website → https://mckaymortgageco.com/

If something in this episode made you think, question, or laugh, don’t let it stop here.

Follow Make Yourself at Home and stay part of the conversation:

Follow Deana Brummett:

Website → https://athomeinthecarolinas.com/

Instagram → https://www.instagram.com/AtHomeintheCarolinas/

Facebook → https://www.facebook.com/HomeintheCarolinas

FAQ

What Is the Home Buyer’s Privacy Protection Act?

The Home Buyer’s Privacy Protection Act - also called the trigger lead bill - is a federal law that prohibits credit bureaus from selling consumer mortgage data without explicit opt-in permission. It went into effect in early 2025 and passed unanimously in both chambers of Congress.

What Is the Difference Between a Mortgage Broker and a Direct Lender?

A mortgage broker like Brendan McKay at McKay Mortgage works with multiple wholesale lenders to find the best rate for a borrower. A direct lender or bank funds loans from their own capital. Wholesale pricing - which brokers access - is typically lower than retail pricing, which means a well-run brokerage can often offer better rates, even accounting for the broker’s compensation.

Does It Matter If I Use a Local Loan Officer?

For a purchase transaction, yes. A local loan officer’s reputation is tied to the community where you are buying. Real estate agents in that market know who closes on time. That accountability creates a real performance incentive that a national call center cannot replicate. Whether you’re weighing new construction vs resale or trying to understand how South Charlotte neighborhoods differ, the lender relationship matters just as much as knowing the market.

Apply to Be a Guest on “Make Yourself at Home” Podcast

If you serve the real estate industry - through staffing, lending, brokerage, technology, or advisory - and help agents grow smarter, not harder...

Let’s spotlight your insights.