Most people think buying a home starts with scrolling listings and comparing prices. But the smartest move you can make happens long before you ever walk through a front door, and it starts with getting your finances right. The problem is, financial literacy for homebuyers is never taught in school, and the internet is full of noise designed to confuse rather than educate.

I had the pleasure of sitting down with Annika Lynn of Movement Mortgage on my podcast. Annika doesn’t just help people get loans, but looks at their entire financial picture and builds a strategy for long-term wealth. In our conversation, she shared her "four legs of the table" framework, broke down why interest rates should not dictate when you buy, and offered the kind of practical money advice that most lenders never talk about.

Why I Had This Conversation

As someone who has spent nearly two decades in real estate through At Home in the Carolinas, I have watched too many buyers get tripped up by misinformation, like bad advice from social media, misleading lender commercials, and the myth that you need 20 percent down to buy a house. I wanted to bring someone onto the show who could cut through all of that.

Annika looks at your entire financial picture—income, debt, savings, investments—and helps you build a strategy that actually sets you up for long-term success. She has the track record to back it up, too. Within two years of entering the mortgage industry, she was listed among the top lenders in the country.

When someone has walked through the kind of adversity Annika has and turned it into a career built on helping others win financially, that’s a conversation worth having.

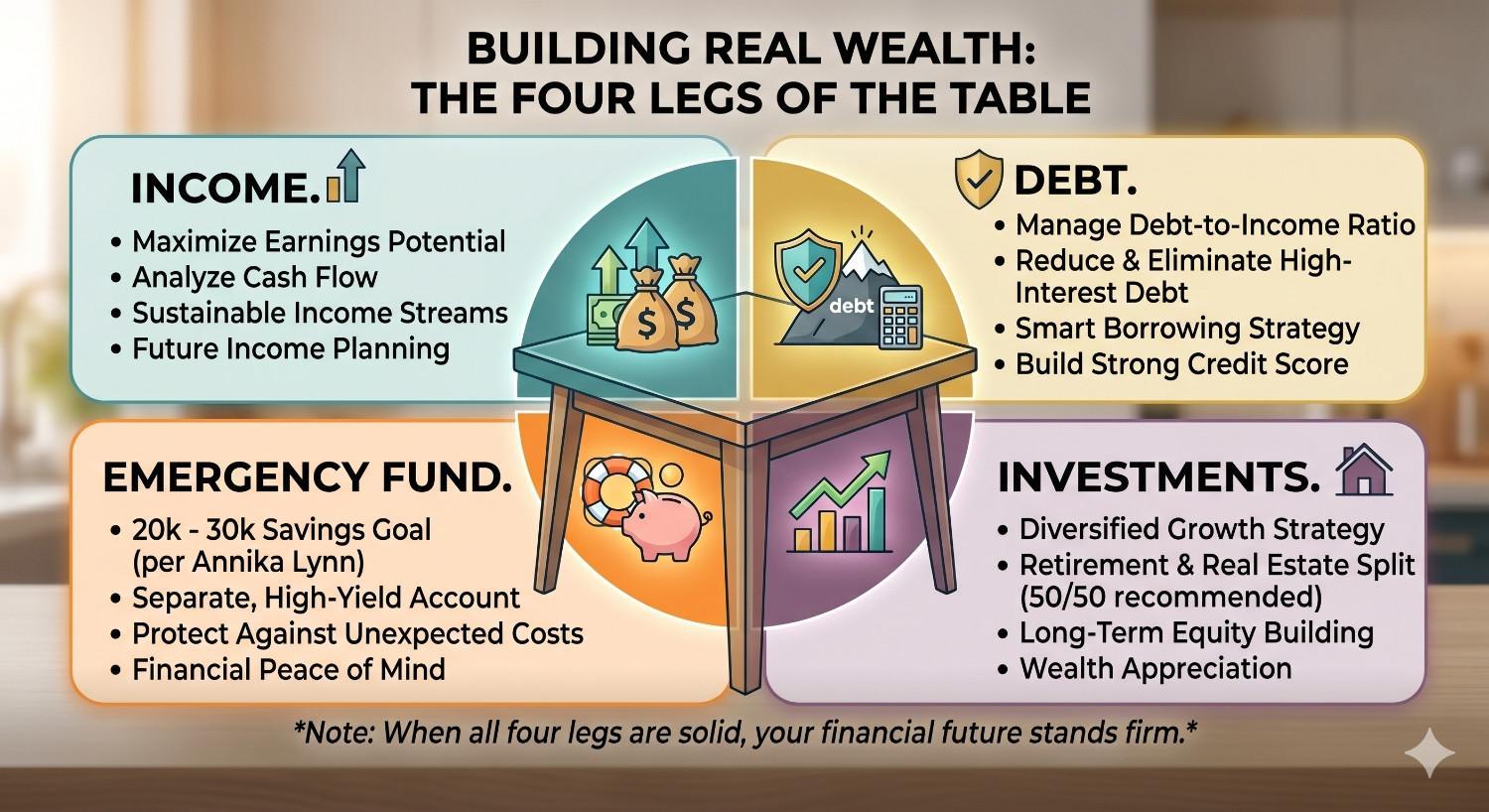

The Four Legs of the Table: A Framework for Financial Literacy for Homebuyers

One of the most powerful things Annika shared is what she calls the "four legs of the table." She tells every client the same thing: she does not really care about their loan. That’s just one tiny puzzle piece. What she cares about is their whole financial picture, and she breaks it into four pillars: income, debt, emergency fund, and investments.

"I don't really care about your loan. That's just one tiny puzzle piece in your whole financial picture. I care about your whole financial picture. I call it the four legs of the table — income, debt, emergency fund, and investments — and I look at each leg to give clients guidance on how to properly handle the money they have so that it grows."

–

On the investment side, she recommends a roughly 50/50 split between retirement accounts and real estate. The idea is that all four legs need to be solid for the table to stand. If your debt is out of control or you have no emergency fund, even the best mortgage rate in the world will not save you from financial stress.

When I work with clients through the process of buying a home, I want them to have this foundation before they ever make an offer.

Why Interest Rates Should Not Drive Your Home Purchase Decision

Annika asked me point-blank what the interest rates were on every home I have ever owned. And honestly, I barely remembered. She does this with her clients, too. She asks them their credit card rate and their student loan rate, and they never know.

Her point is sharp: you do not build wealth based on an interest rate. You build wealth by using money properly. People fixate on rates because it is the only question they know to ask.

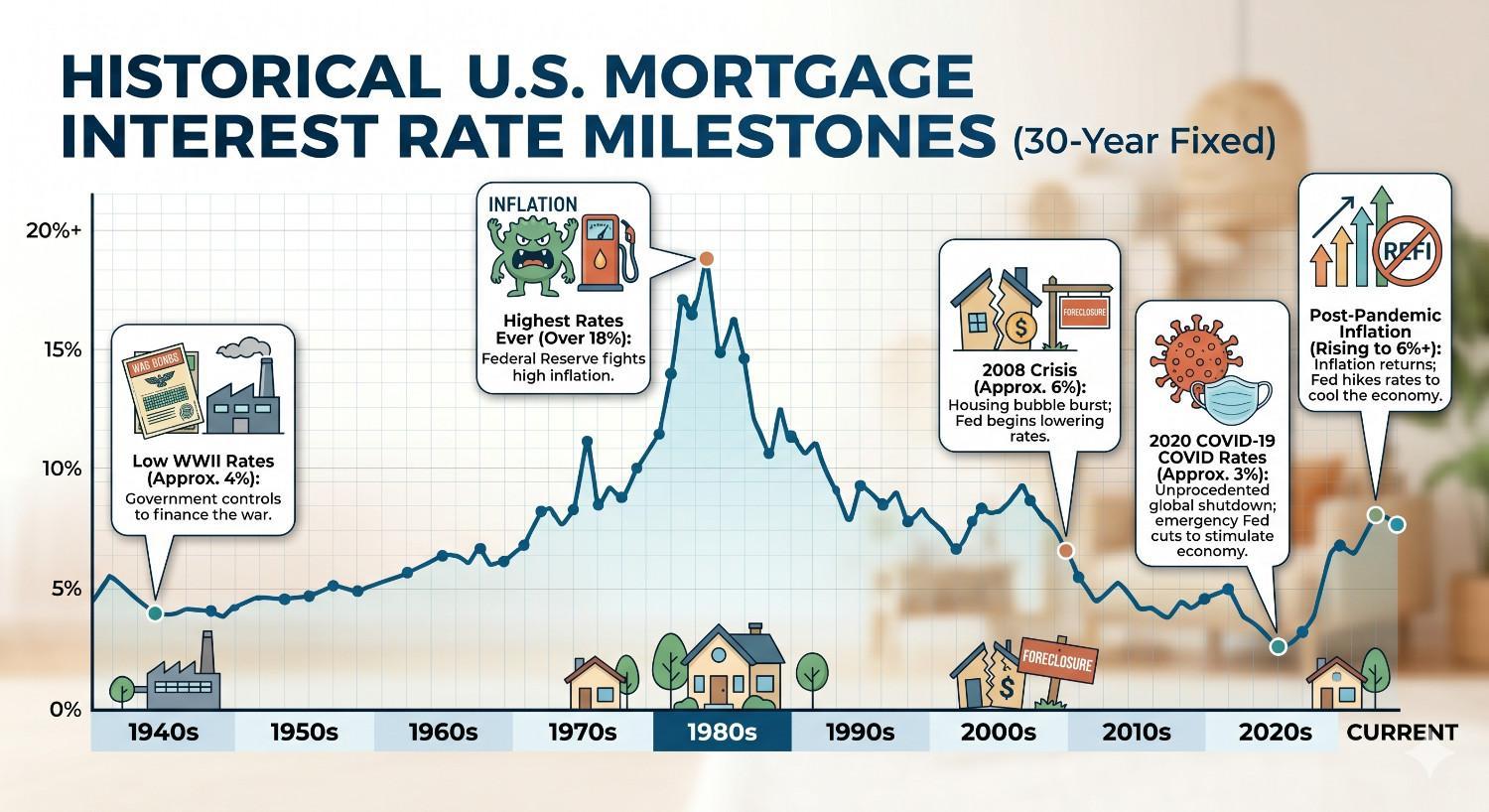

She also put the 3% rate era into historical context. The last time rates were that low before 2020 was during World War II, an 80-year gap driven by economic catastrophe. Waiting for that to happen again is not a financial strategy.

And here is the critical distinction: your interest rate is temporary, but your purchase price is permanent. When rates come down, a good lender will refinance you out of it. But the price you locked in? That is yours forever.

Building Your Team and the Power of a Local Mortgage Lender

Annika said that choosing a mortgage lender is like building a team. You need someone who thinks as you do, shares your financial worldview, and tells you the truth even when it’s uncomfortable. A Charlotte-area mortgage lender who is local has skin in the game. They’re afraid of running into you at the grocery store if they didn’t do right by you.

"You cannot build wealth without owning real estate. And our industry, my side in particular, is so shrouded with smoke and mirrors. The most important thing a client can do is find a lender and a real estate agent they can trust implicitly — somebody who's going to tell you the truth, because there is no truth on the internet."

–

She contrasted this with big box lenders who throw out pre-approval letters to anyone without truly vetting their finances. When Annika writes a pre-approval, she has already tried to underwrite the file herself. Her goal is to answer every question her underwriters will ask before they ask it.

Smart Money Habits That Protect Your Emergency Fund for Homeownership

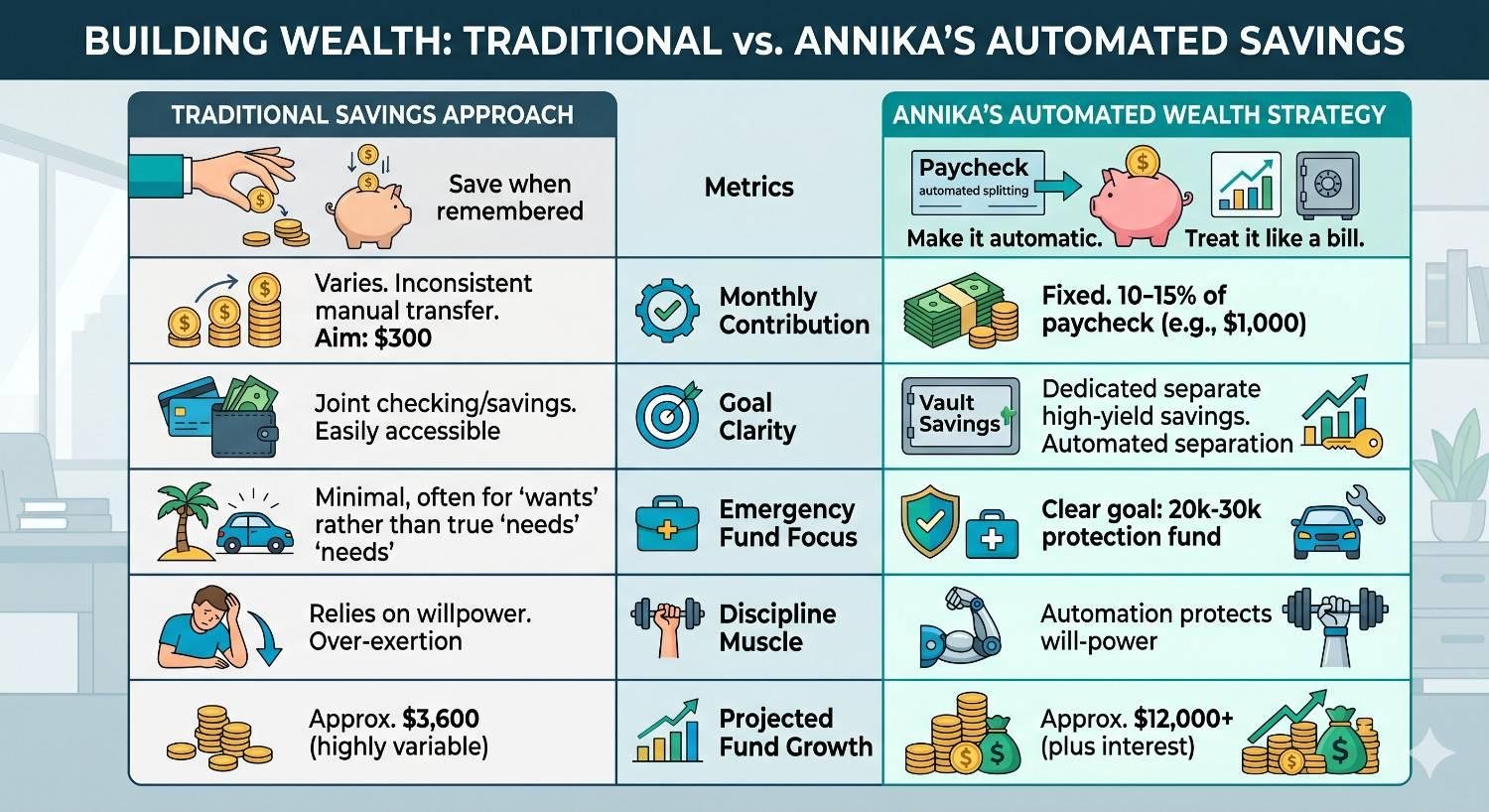

Annika told me that a thousand-dollar emergency fund for homeownership doesn’t cut it; twenty to thirty thousand dollars is more realistic. And, the way to get there is through automation. Set up your paycheck to siphon 10 to 15 percent into a separate savings account at a different bank, because as she put it, money is like a puppy—it wants to play with its friends.

She also talked about using a credit card as a "drinking straw." All spending flows through it, but she pays it off every couple of days. It builds credit, tracks spending, and keeps her from touching savings. She also recommended high-yield savings accounts for the real emergency fund, kept completely separate from working capital.

What Changed for Me After This Conversation

"Self-control is the only muscle that gets weaker with use. You're not going to remember to put money in savings every paycheck. You've got to make it automatic. You can save more than you think, and you need more than you think."

–

After sitting down with Annika, I walked away thinking about how many of my clients could benefit from hearing this before they ever start looking at houses. We spend so much time in real estate talking about neighborhoods, square footage, and school districts, but the foundation of every successful purchase is financial health.

What I now tell my clients is this: before you fall in love with a house, fall in love with a plan. Find a lender who will look at your whole picture, not just your loan amount. Build an emergency fund for homeownership. Kill your debt. And, stop waiting for interest rates to magically drop. The best time to buy is when your finances are ready, not when the market tells you to.

That is building wealth through real estate the right way!

Want to hear my full conversation with Annika Lynn of Movement Mortgage on building wealth through homeownership?

Frequently Asked Questions

Why shouldn't I wait for lower interest rates to buy a home?

Your interest rate is temporary—you can refinance when rates drop. But your purchase price is permanent. Higher rates mean less competition and lower prices, which often puts you in a better position long-term. Waiting costs you appreciation and equity while rent continues to climb.

What is a temporary rate buydown, and how does it help first-time buyers?

A temporary rate buydown uses seller concessions to lower your interest rate by one or two percentage points during the first years of the loan. It makes monthly payments more affordable while your income grows.

How much should I have in my emergency fund before buying a home?

A thousand dollars is not enough. Aim for twenty to thirty thousand dollars in a separate high-yield savings account. Automate your savings so 10 to 15 percent of each paycheck goes directly into that fund. This cushion prevents routine expenses from becoming financial crises after you close.

Apply as a Guest on the Make Yourself at Home Podcast

The real estate and lending landscape is shifting fast. Interest rates, market conditions, and buyer expectations are all evolving, and the professionals navigating them every day have stories worth sharing.

If you’re working in real estate, mortgage lending, financial planning, or any related field, and you’re solving real problems for real people, join me on my show!

Make Yourself at Home is produced by Icons of Real Estate, the #1 Real Estate Podcast Network. If you are a real estate professional, apply to be a guest speaker across the network!