One of the biggest frustrations I hear from buyers every single week is the belief that they need $80,000 sitting in the bank before they can even think about owning a home. That myth keeps good people stuck in a cycle of renting, and it’s costing them real money every year they wait. I wanted to have a conversation with someone who could speak to both sides of the equation, which led me to Andrew Postell of CrossCountry Mortgage.

On a recent episode of Make Yourself at Home, Andrew and I explored how everyday buyers can turn homeownership into a long-term wealth-building strategy. We walked through the biggest insights from our conversation and what stood out to me as a real estate agent who sees these challenges firsthand every day.

Why I Had This Conversation

As a real estate investor who started with almost nothing, a licensed mortgage professional, and now a recognized top producer specializing in different types of mortgage loans, Andrew is the kind of professional I wanted to share real-world experience with my listeners.

Running At Home in the Carolinas, I see every day how the right guidance at the right time changes lives, and Andrew’s real estate wealth-building strategies are exactly the guidance people need right now.

Whether you’re trying to figure out buying a home for the first time or looking to turn your current property into the foundation of something bigger, what Andrew shared is worth sitting with.

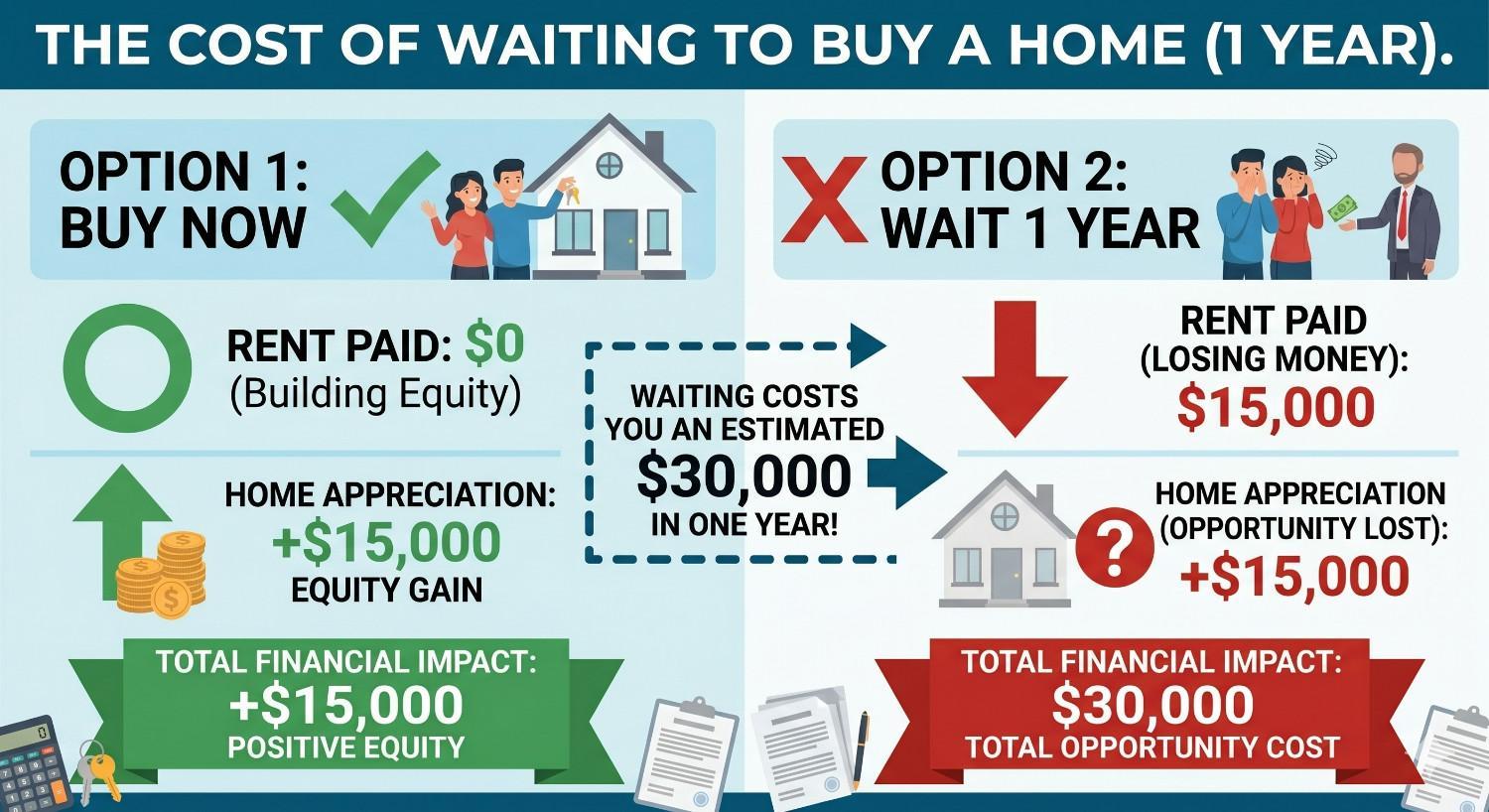

The Real Cost of Waiting to Buy a Home

Andrew said something during our conversation that stuck with me: the most expensive mistake a first-time buyer can make is simply waiting.

Here’s the math that most people do not think about. If you’re renting at $1,500 a month, you’re handing a landlord $12,000 to $15,000 a year that you’ll never see again. While you’re paying someone else's mortgage, the home you were eyeing has appreciated another $10,000 to $15,000 in value. That means in a single year of waiting, you have effectively lost $30,000 in combined opportunity.

I tell my clients this constantly. People say they’re waiting for interest rates to drop, but home prices will always outpace a half-point rate reduction. If you wait for rates to fall half a percent, the home you wanted has already climbed well past whatever you would have saved on your monthly payment.

There are down payment assistance programs available right now that can get buyers into a home with very little out of pocket. Andrew himself used one when he bought his first property. The trade-off is usually a slightly higher interest rate, but that’s a rate you can refinance later. The door is open, and you’re building equity instead of paying rent.

Andrew specializes in connecting buyers with multiple grant options and mortgage loans that fit their situation. One of the things I appreciated most was that he did not sugarcoat it. He said homeownership is harder now than it has ever been. But harder does not mean impossible, and programs exist specifically to help people in that position.

"If you own a home today, in five years, you can be very thankful that you own it. It is not going to get any easier next year or the year after that. I just want to encourage everybody to think about consulting with your agent, consulting with your loan officer about whether you can even make this possible. And if they are good, they will give you a little plan about how you can get it accomplished."

–

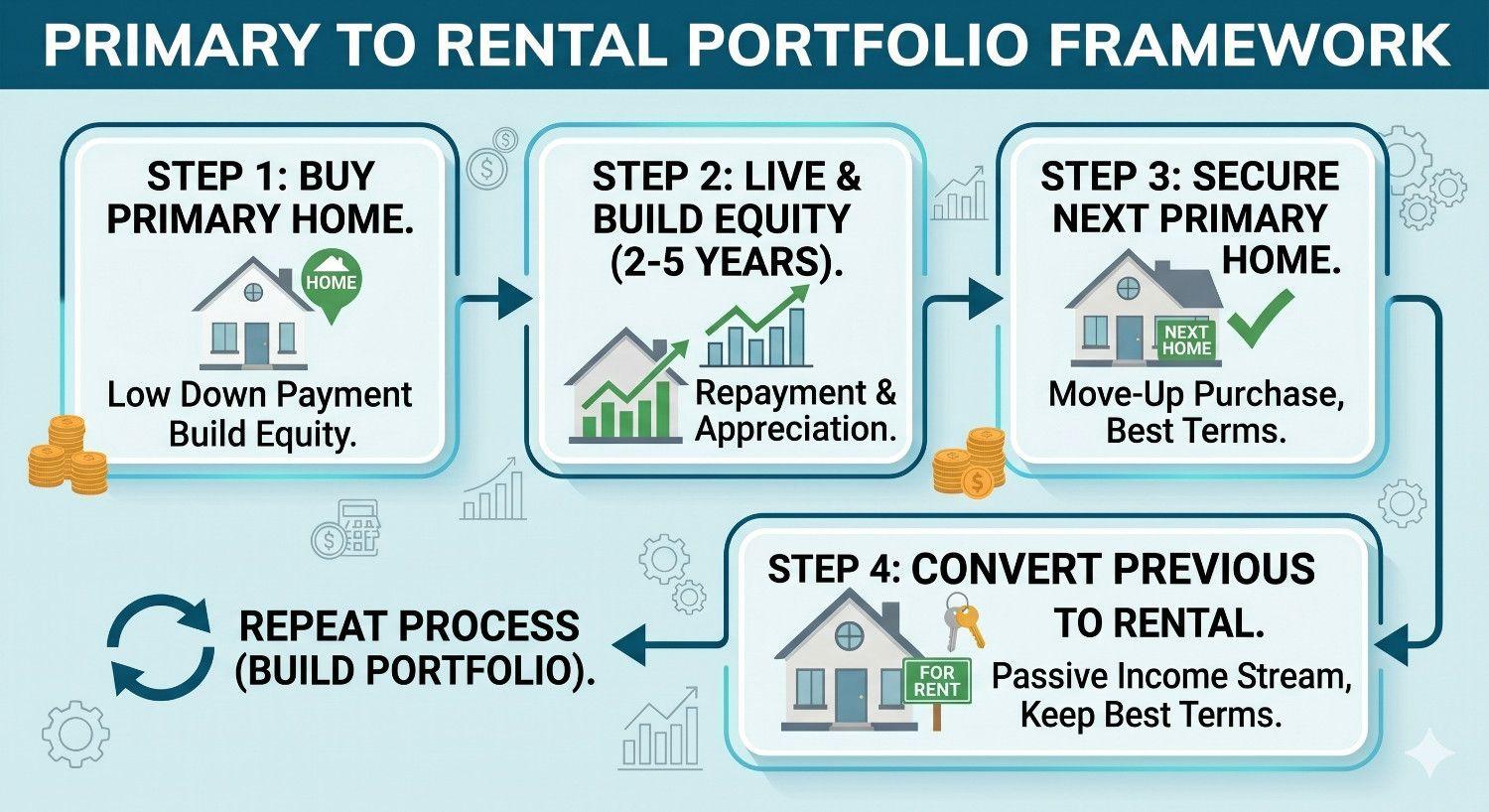

Turning Your Primary Home Into a Rental Portfolio

Andrew shared a strategy that completely reframed how I think about first-time buyers and long-term planning.

His uncle bought his primary home, lived in it, then kept it as a rental when he moved to his next home. By the time he retired, he owned seven properties and was financially set for life.

Andrew did the same thing. His first home was a cinder block house where he rented out the rooms. When he moved out, he kept it as a rental. That one decision started a chain that led him from $4,000 in savings after leaving the Marines to becoming a millionaire through real estate.

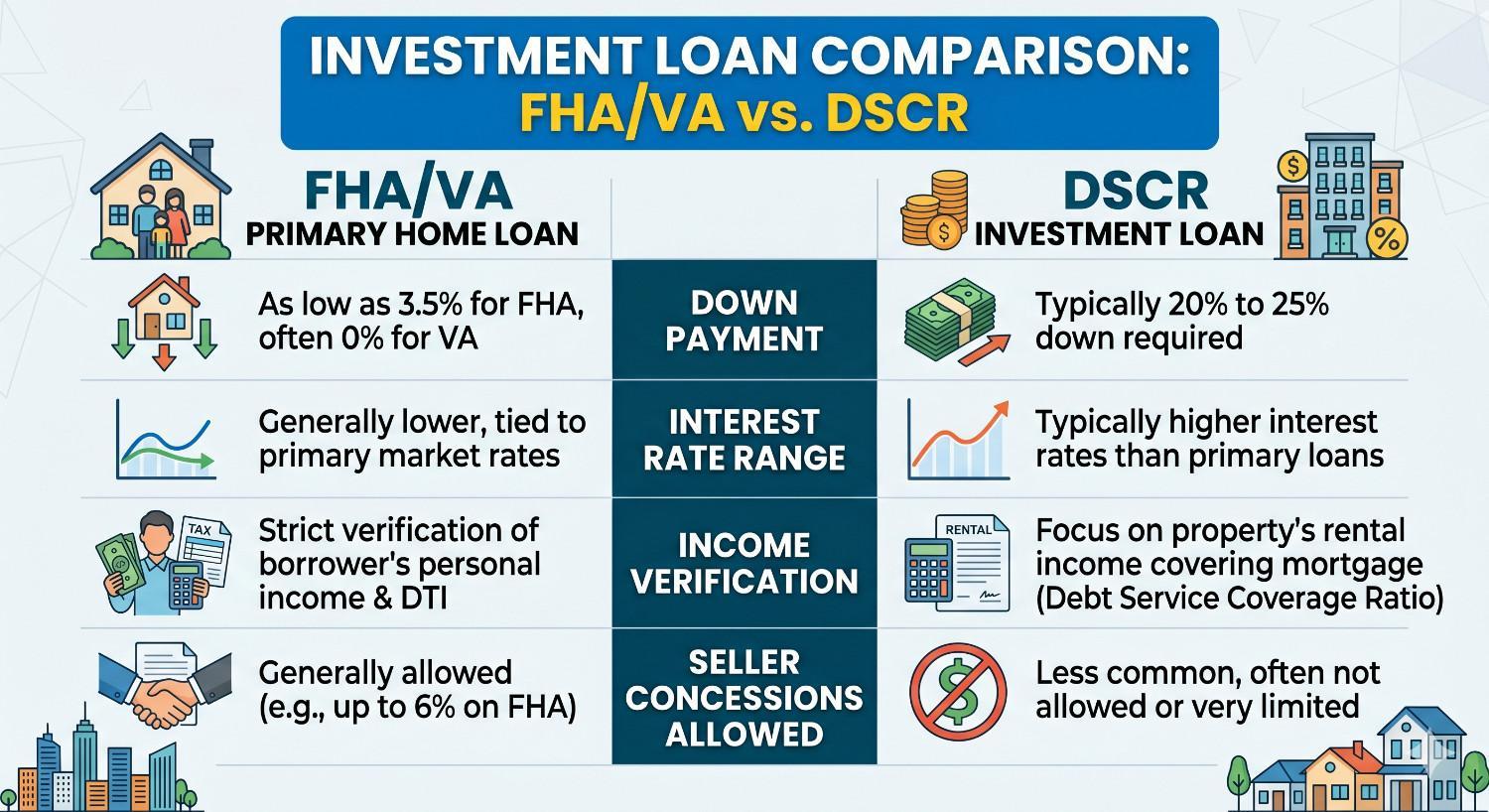

DSCR Loans and the BRRR Method: What Aspiring Investors Need to Know

Once buyers are ready to scale beyond their primary home, Andrew introduced two concepts that every aspiring investor should research.

DSCR loans for real estate investors are essentially commercial-style loans where the property's rental income needs to cover the mortgage payment. If your payment is $1,995, your rent needs to be at least $2,000. The advantage is that there’s no personal debt-to-income ratio involved, which is huge for self-employed borrowers or investors who want to hold properties in a business entity.

"Three-bedroom, two-bath homes below the median home price — that is where your tenants live. That is where the working-class people, the blue-collar families are. They are good tenants. They pay on time. They live there for a long time. Give them a great home because they were living somewhere that was not so good, and when they see your property, they will rent it."

–

The catch is that DSCR loans typically require 20 to 25 percent down, which is why Andrew also recommends learning the BRRR method. This approach targets off-market properties that need significant work, uses a temporary loan to acquire and fix them, and then refinances into a DSCR loan once the property is stabilized.

What Changed for Me After This Conversation

What stuck with me most was not a single strategy or loan product. It was Andrew's perspective on pace. Only four percent of Americans own two homes. That statistic alone tells you how hard it is. But Andrew did not frame it as discouraging. He framed it as proof that even small progress puts you ahead of almost everyone.

"It is not a race. It is not a competition. Let us say you bought one home every five years. You are going to be a millionaire. It is okay. Just take your time. Imagine if you get retired and you have four properties and they are paid off. Save money, live a little bit beneath your means, support your family, have a great job. These things will lead to better things later."

–

I hear from buyers constantly who feel paralyzed by what they see on social media—people claiming they bought 10 homes in a day. Andrew and I both agree that building wealth through real estate is about consistency, not speed. Find the right team. Start with the home you can afford today. Save a little, stay focused, and let time do the heavy lifting.

That is the message I want every person listening to walk away with, and it is the approach I take with every client I work with as their agent.

Want to hear my full conversation with Andrew Postell of CrossCountry Mortgage for more real estate wealth building and rental property investment tips?

Frequently Asked Questions

How much money do I actually need to buy my first home?

With the right down payment assistance programs, you may need as little as $1,200 out of pocket. Government-backed loans, like FHA loans and VA loans, offer down payments as low as three to five percent, and grants can cover a significant portion of that.

What is a DSCR loan, and who qualifies for one?

DSCR stands for “debt-service coverage ratio.” DSCR loans are designed for real estate investors and require that the rental income on the property covers the mortgage payment. Expect to put 20 to 25 percent down.

What type of rental property gives the best return on investment?

Target three-bedroom, two-bath homes below the median home price in your market. These properties attract stable, long-term tenants and are easier to rent than higher-priced homes.

Apply as a Guest on the Make Yourself at Home Podcast

Real estate is personal. Whether you’re navigating your first purchase, building a rental portfolio, or helping clients find their next home, your experience matters. If you’re working in the industry and have insights worth sharing, I’d love to have you on my show!

Make Yourself at Home is produced by Icons of Real Estate, the #1 Real Estate Podcast Network. If you’re a real estate professional, apply to be a guest speaker across the network!