Most homeowners pay their premiums faithfully for years, and then, the moment they actually need to file a claim, they discover the system was never designed to work in their favor. I’ve seen it up close with my own clients, and I lived it personally when my mother spent two years and $150,000 rebuilding her house after a tenant-caused flood. That experience is part of why I knew I had to sit down with Andy Gurczak from AllCity Adjusting and bring this conversation directly to you.

Andy is the Founder and CEO of AllCity Adjusting, a nationwide public adjusting firm operating in 42 states. He exclusively advocates for property owners, never insurance companies, and has spent his career learning exactly how claims are won, lost, denied, and underpaid. This episode of Make Yourself at Home is one of the most practical conversations I’ve had on protecting the biggest investment most people will ever make.

Here’s what we cover:

-

Why the insurance claims system is structured to delay and underpay

-

The specific words that can get your claim denied, even if it’s legitimate

-

A real case where a $10,000 check turned into $32,000

-

The policy add-ons most homeowners have never heard of

-

Why investors need a public adjuster on their team

Andy Gurczak of AllCity Adjusting: Why I Had This Conversation

I started Make Yourself at Home because there are 25,000 real estate agents in the Charlotte Metro alone, and almost nobody is speaking directly to the consumer. Most of what’s out there is agents talking to agents. My goal is to give everyday buyers, sellers, and homeowners the vocabulary and awareness to protect themselves.

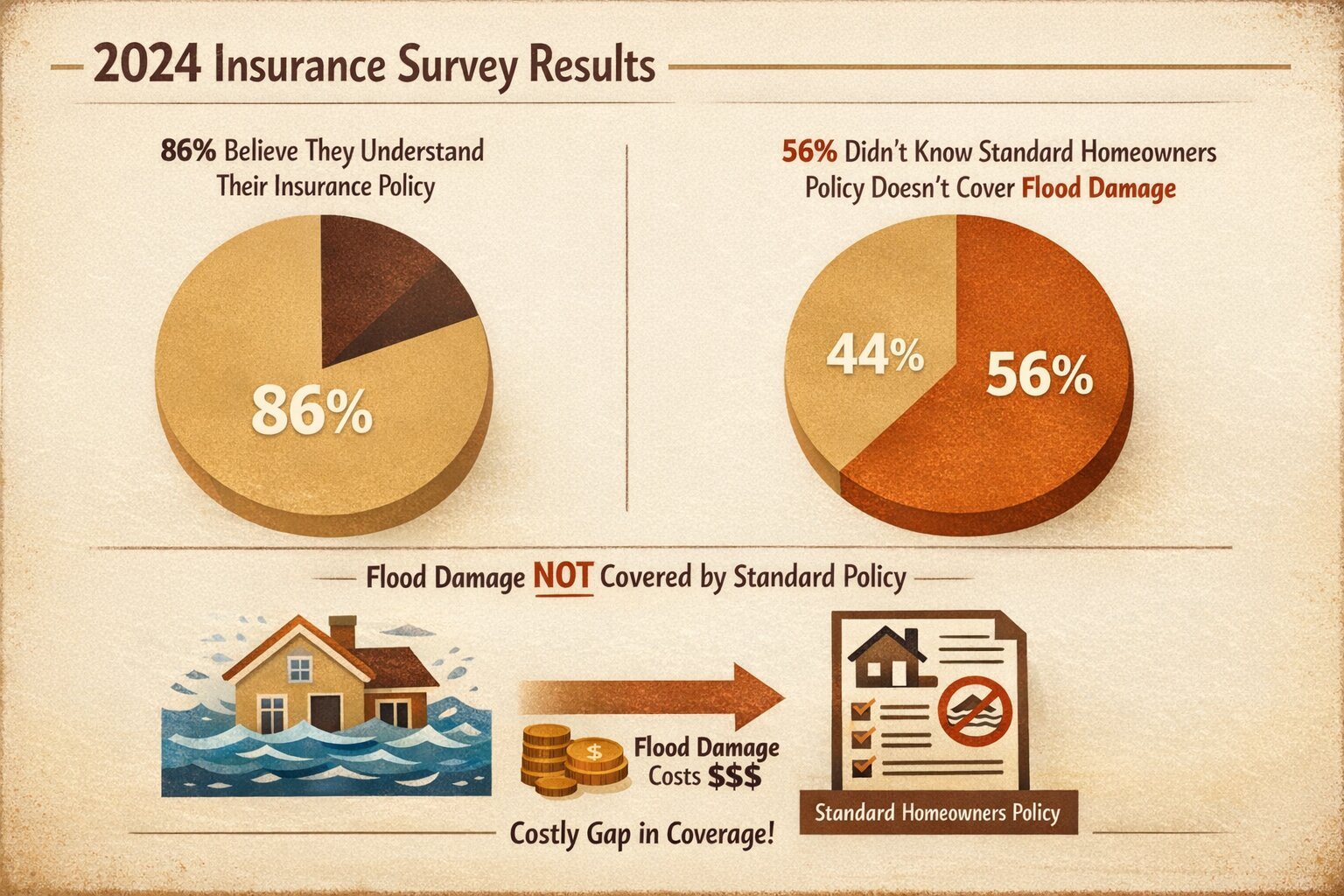

A 2024 industry survey found that while 86% of consumers believed they understood their insurance policy, 56% did not realize a standard homeowners policy typically does not cover flood damage, a gap that costs people thousands when disaster actually strikes, according to the Insurance Information Institute.

Why the Insurance Claims System Isn’t Built in Your Favor

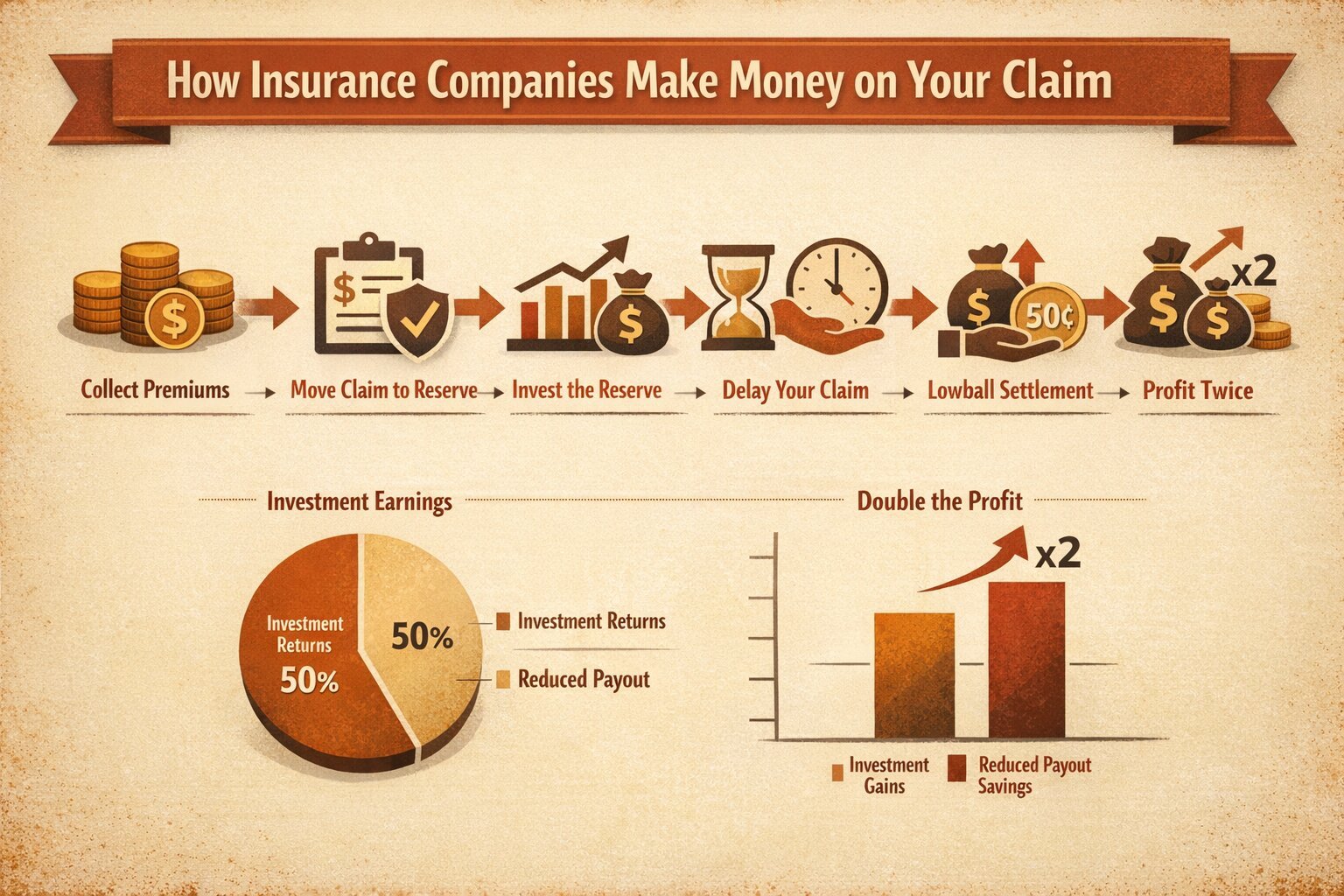

Andy was direct about this from the start. The claims process isn’t designed for your convenience. It’s designed to protect the insurer’s bottom line.

Insurance companies collect premiums, but the real money comes when a claim is moved into reserve. That reserve gets invested.

The longer your claim is delayed, the more the insurer earns on it. And if they can settle at 50 cents on the dollar, they’ve made money twice:

-

On the investment

-

On the reduced payout.

The adjuster sent by your insurance company works for them.

Your agent sells policies, Andy said it plainly:

-

Agents have never seen the claims system

-

They don’t know what happens inside it,

-

And they typically don’t have a copy of your policy on hand. That’s not your team. That’s the other team.

The Words You Use Can Make or Break Your Claim

“A lot of people calls us and they say, ‘we had a flood in the basement.’ You’re going to jot everything down and say, well, this is denied, sorry, sir, you don’t have flood coverage. But I had a pipe burst and the water’s everywhere. I called it a flood because it’s a lot of water. I don’t know. I’ve flooded my basement, right? But pipe breaks, frozen pipes, flood’s not covered. So it’s using the right stuff, using the right words. A lot of people are making the mistake of saying the wrong things and then talking too much.”

— Andy Gurczak, Founder & CEO, AllCity Adjusting

This was one of the most eye-opening moments in the episode. The exact words you use when reporting a claim can determine whether it gets covered at all. Calling a pipe burst a “flood” because that’s what it looks like, can trigger an immediate denial since flood coverage is a separate policy most homeowners don’t carry.

Beyond word choice, Andy warned that oversharing is a serious liability.

Mentioning the following can give the insurance company grounds to reduce or deny the claim:

-

DIY electrical work

-

Delayed maintenance

-

A relative staying at the property

The rep on the phone isn’t there to help you build your case. They’re documenting information that can be used against you.

|

❌ Don’t Say This |

✅ Say This Instead |

|

We had a flood in the basement |

We had a pipe burst |

|

The toilet overflowed / the sewer backed up |

The toilet clogged and overflowed [not a backup] |

|

My cousin was staying here / I rewired that myself |

Say only what’s necessary. Less is more. |

Andy’s advice: keep it factual, keep it brief, and bring in a public adjuster insurance claims expert before you say more than necessary. That one step can be the difference between a denied claim and a full payout.

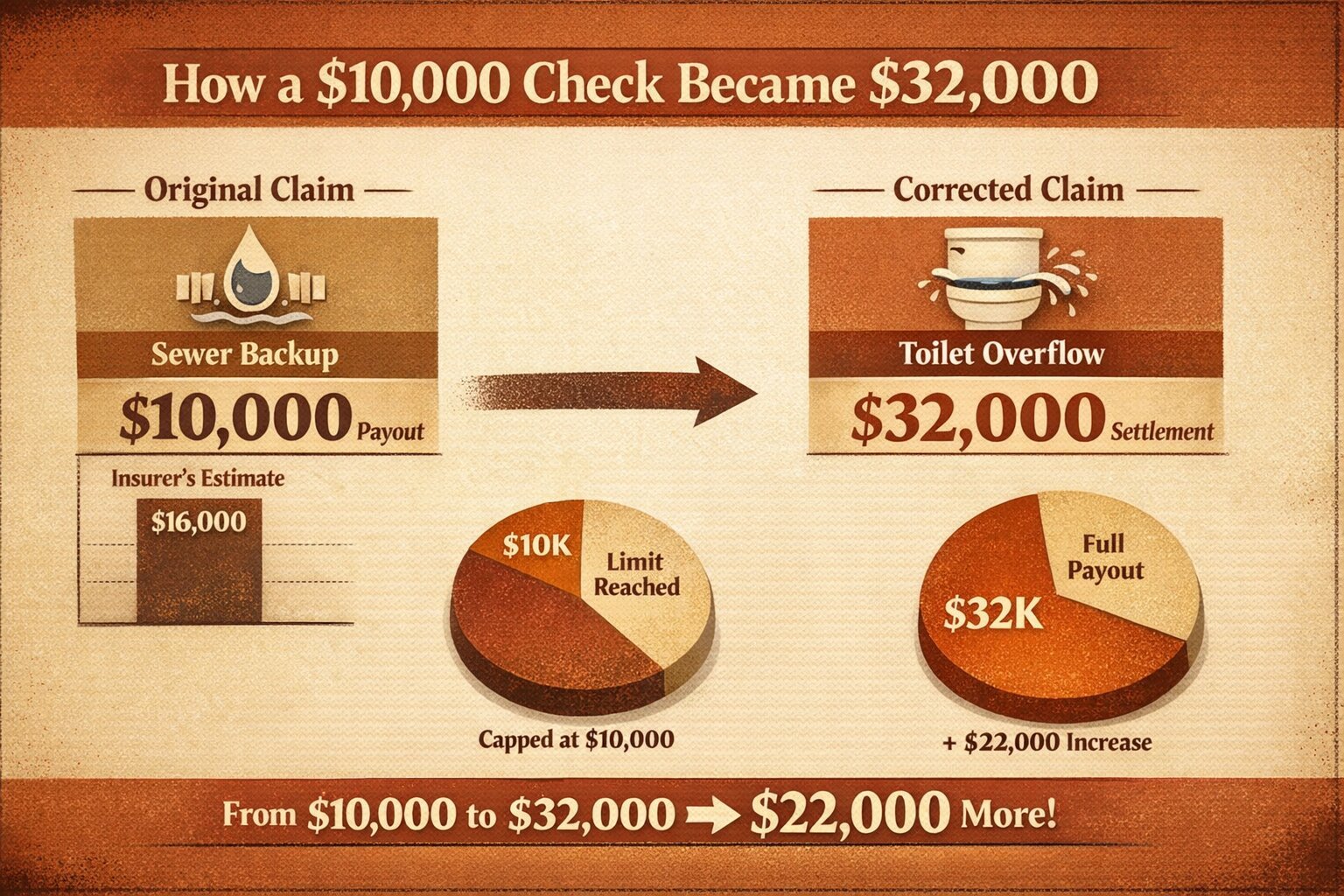

A Real Example, How a $10,000 Check Became $32,000

Andy shared a case from just a week before we recorded, and it made everything click. A client received a $10,000 check from their insurer for what was classified as a sewer backup. The insurer’s own estimate was $16,000, but the policy’s sewer backup limit capped the payout at $10,000.

When Andy’s team reviewed it, they found the actual event was a toilet clog that overflowed, a meaningfully different classification. By correcting the terminology and rewriting the estimate, the claim was overturned and settled at $32,000. That’s more than triple the original check, and a $22,000 difference that came down entirely to word choice and having someone who knew how to fight it.

Water damage is not some rare, freak-event claim. According to ConsumerAffairs’ analysis showing water damage and freezing accounted for nearly 24% of all homeowners insurance claims in 2021, with the average claim topping $12,500, this is one of the most common claims homeowners will face, and also one where a misclassification can wipe out most of the payout.

What Homebuyers and Investors Should Check Before It’s Too Late

"When it comes to the insurance industry, especially the claims we see, insurance companies stopped doing inspections a long time ago. Most don’t inspect the property before they insure you. So the inside of the property, that’s obviously the home inspector’s job. But I would be looking at: has there been any water damage? If I have a finished basement, is there a chance there might be another water backup? Also, how old is the home? If the home is 100 years old, you might want a service line endorsement. And law and ordinance, if your home is 50 years old, everything’s changed every 10 years. You had a water loss, two floors need to be gutted, and now the city says the electrical has to be upgraded and you need fire sprinklers. Well, that’s law and ordinance coverage. If you don’t have coverage for it, that’s out of pocket."– Andy Gurczak, Founder & CEO, AllCity Adjusting

Here’s what Andy told me to look for:

|

Coverage Type |

What It Covers |

Who Needs It Most |

Risk If Missing |

|

CLUE Report Review |

Full claim history tied to the address |

All homebuyers |

Higher premiums or uninsurable property |

|

Service Line Endorsement |

Main sewer line damage (tree roots, deterioration) |

Owners of older homes |

Full sewer replacement out of pocket |

|

Law and Ordinance Coverage |

Code-mandated upgrades after a covered loss |

Homes 20+ years old |

$30,000+ out of pocket for code upgrades |

|

Roof Age Clause Awareness |

Whether policy pays ACV vs replacement cost |

Anyone with a roof 10+ years old |

Payout leaves $4,000 on a $20,000 roof |

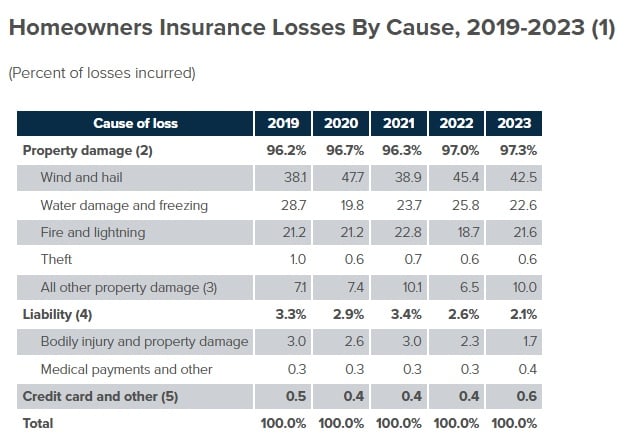

Roof claims sound simple until you see how common and expensive they’ve become. According to III data showing wind and hail accounted for 42.5% of homeowners insurance losses in 2023, with claims averaging nearly $14,747 over the 2019–2023 period, meaning the coverage details in that roof age clause matter enormously.

Here’s the rest of the top causes of insurance loss by homeowners, as compiled by the Insurance Information Institute.

Why Investors Especially Need a Public Adjuster on Their Team

Andy made it plain: a public adjuster on your team is like a tax accountant or real estate attorney. You don’t wait for a crisis to find one.

For investors with multiple properties, the complexity multiplies fast. Andy’s firm advises some clients not to file at all if the damage won’t clear the deductible, because unnecessary claims can affect future premiums and coverage eligibility.

-

They assess whether a claim is worth filing before you pick up the phone

-

They know the terminology that gets claims covered instead of denied

-

They negotiate the settlement, not just review it

-

They’re paid on contingency, so their incentive is aligned with yours

For smaller losses, a good public adjuster will tell you honestly when you don’t need one.

What Changed for Me After This Conversation

Before this episode, I treated insurance as a checkbox in a real estate transaction. Now I see it as one of the most consequential decisions a buyer or investor makes. The CLUE report home buying conversation, the policy review, the endorsements, the roof age clause are now part of how I talk to every client.

The team of Andy Gurczak at AllCity Adjusting offers free policy reviews to anyone who sends in their policy. No client relationship required. If you’ve never had someone look at your coverage from a claims standpoint, not a sales standpoint, this is a genuinely rare opportunity. Reach them at allcityadjusting.com.

FAQ: What Homeowners and Investors Ask About Insurance Claims

What is a public adjuster and how are they different from an insurance adjuster?

A public adjuster works exclusively for you, the policyholder, not the insurance company. The adjuster your insurer sends represents their interests. A public adjuster reviews your policy, documents the damage, and negotiates to maximize your settlement. If your insurance claim denied coverage unfairly, a public adjuster can build the case to challenge that decision. As Andy explained in the episode, the adjuster from your insurer and the vendors they recommend are all working for the same team, and it’s not yours.

When should I call a public adjuster?

Andy recommends calling before you say much to your insurance company, especially on large or complex claims involving fire, water, wind, or roof damage. The sooner you bring in an advocate, the less chance of a misstep in terminology or documentation that could reduce or eliminate your payout.

What is a CLUE report and why does it matter when buying a home?

CLUE stands for Comprehensive Loss Underwriting Exchange. It’s a record of every insurance claim ever filed against a property address. The history stays with the address, not the previous owner. A home with repeated claims for water damage or roof issues can be harder to insure and more expensive to cover.

What policy add-ons does Andy recommend most often?

Based on our conversation, the three most overlooked are: a service line endorsement (especially for older homes), law and ordinance coverage (critical if your home is more than 20–30 years old), and sewer backup coverage. These are often inexpensive additions that can prevent enormous out-of-pocket expenses after a loss.

Is there such a thing as a free roof?

No. When storm chasers promise a free roof, remember you’ve already paid premiums for that coverage. The claim itself can raise your rates or affect future insurability. Have a public adjuster assess whether the payout will actually exceed your deductible before filing.

Keep the Conversation Going

If you want to make sure your coverage is actually protecting you, reach out to Andy Gurczak and the AllCity Adjusting team below:

-

Website → https://allcityadjusting.com/

-

LinkedIn → https://www.linkedin.com/in/andy-gurczak-528b9b64

If something in this episode made you think, question, or laugh, don’t let it stop here.

Follow me at Make Yourself at Home and stay part of the conversation.

-

Website → https://athomeinthecarolinas.com/

-

Instagram → @AtHomeintheCarolinas

-

Facebook → HomeintheCarolinas

Apply to Be a Guest on “Make Yourself at Home” Podcast

If you serve the real estate industry through staffing, lending, brokerage, technology, or advisory. And you aim to help agents grow smarter, not harder…

Let’s spotlight your insights.